Heading Into BOJ: Overnight Media Reports Say July Hike, While JPY Hits Markets Again

Heading Into BOJ: Overnight Media Reports Say July Hike, While JPY Hits Markets Again

Multiple media outlets say Bank of Japan will hike policy rates to 0.25% at today's July 2024 Policy Meeting. JGB tapering in focus. USDJPY 152 in sight as MOF's new FX Meddler Mimura's tenure begins.

Thoughts and takes on media reports before BOJ - and note, this time is different with release catalyst schedules - 1) official policy statement (around noon), 2) Governor Ueda press conference (3:30PM), 3) AUGUST JGB BUYING SCHEDULE (5pm - POST-Ueda press conference, where actual imminent JGB tapering amounts, if any, will be laid out).

Press Leaks

Later today- Bank of Japan will release their official July 2024 monetary policy statement. That means that these past few hours overnight heading into the day of the policy announcement had been prime time for the BOJ pre-announcements and press leaking protocol. And goodness, did they come in, each with a consistent "message” - Bank of Japan to hike policy rates to 0.25% (from current 0.0% - 0.1% range).

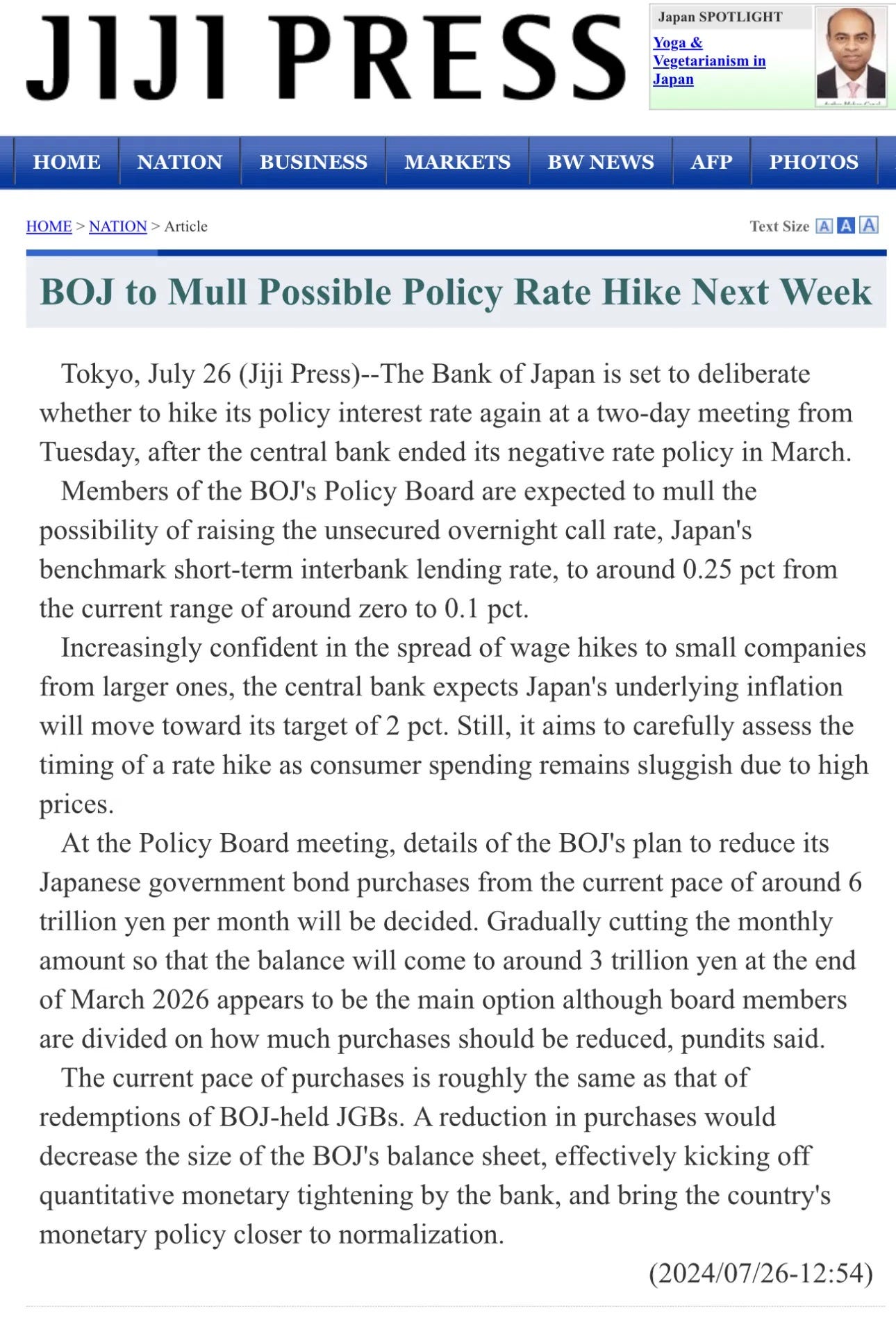

First - JIJI PRESS on July 26th was a few days ahead with this “hike to 025%” headline. But this did not move markets at the time (because its JIJI Press).

The following are the various press releases on BOJ policy speculation in chronological order overnight in Japan hours (non-comprehensive).

11:43 PM - NHK (public broadcast) “BOJ to consider hike to 0.25%”

2:01 AM - Nikkei: “BOJ considering hike to 0.25%”

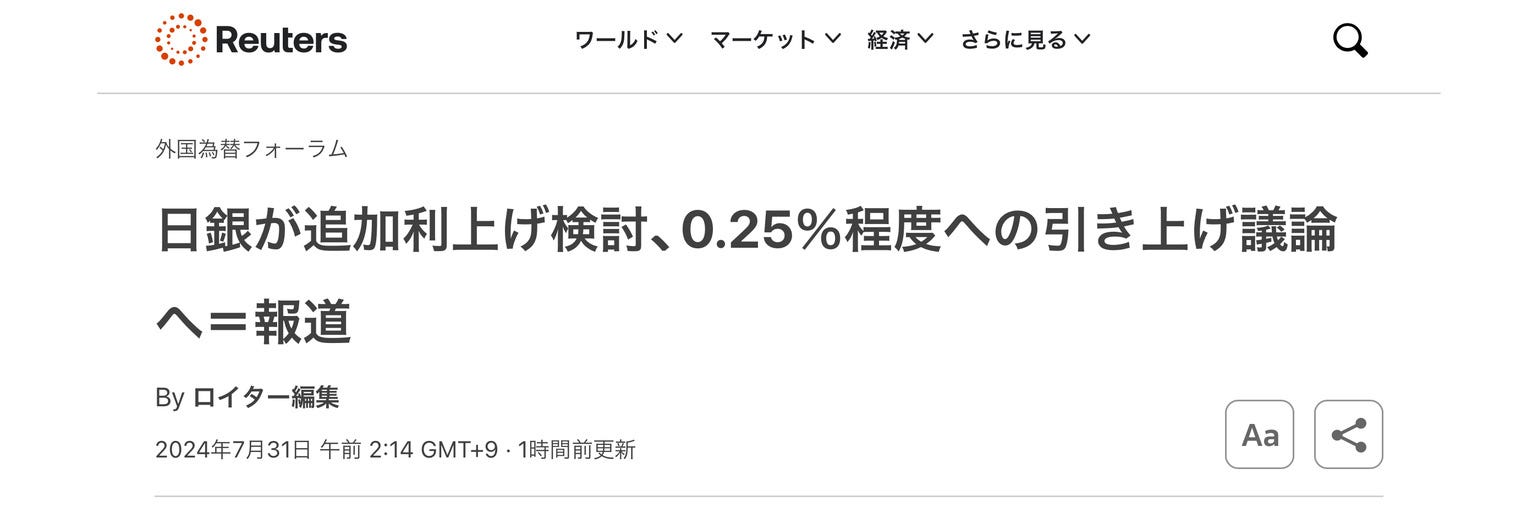

2:14 AM - Reuters Japan: “NHK, JIJI PRESS and other domestic media are saying - BOJ to consider hike to 0.25%”

…and so on.

Here is my personal take: Unlike in similar past instances, this is NOT the Bank of Japan communicating to markets with press leaks.

People here on the ground are talking about “all of these different” media reports coming out over the past several hours. Here is what they're seemingly missing - none of them are different, and they are all just going off of the pre-midnight NHK's “BOJ hike to 0.25% in July.”

So the degree to which “all of these” media reports are to be taken seriously should be carefully considered in the context of - “all of these” is really just one article, one speculative claim, one “inside source” - whatever it is, its just one act of speculation, which is then being echoed by multiple outlets, which can then look or seem like "so much" speculation - but again, it all stems from a single outlet.

That is a very big difference from having different outlets, each of which are saying (truthfully or otherwise) their own version of-

“…according to Bloomberg's sources…”

“…people close to the matter told Reuters…”

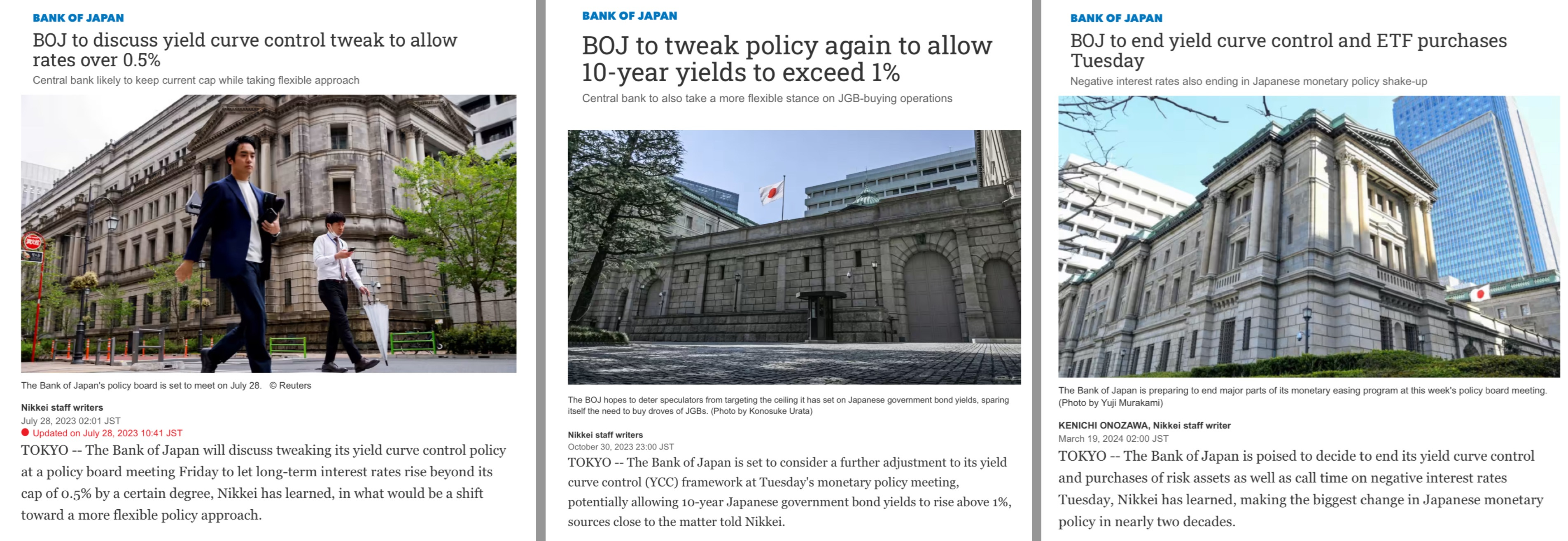

As I've said in many previous BOJ days with accompanying media leaks, there is only one outlet that really matters: Nikkei - who still has their perfect track record of pre-announcing BOJ meeting outcomes within 12 - 24 hours of the official release under Governor Ueda.

Now, Nikkei did also do a 2AM release of “BOJ considering hiking to 0.25%” - but just because Nikkei says prints, doesn't make it “Nikkei-official” - because, as per my article heading into last meeting…

Regarding Nikkei BOJ policy pre-leaks, what I've observed is that the 2 conditions that need to be met are that these articles are authored by “Nikkei staff writers,” AND, Nikkei needs to “learn” something. Like so (from last month)

And every other Nikkei eve-of-shock-policy-change BOJ day under Governor Ueda:

And in this instance, Nikkei hasn't “learned” anything for this one.

I know it sounds very stupid, but I'm just relaying what I have been dead-on accurately observed, noticed, and applied in reading BOJ's public interfacing for years - so you can think its incredibly stupid all you want, all that does is reflect the stupid shit that they do.

A more important point - none of those actually did anything for / to green and red blinking tickers, or if they did, they'd be very hard to detect given the dispersion of these same headlines across several hours.

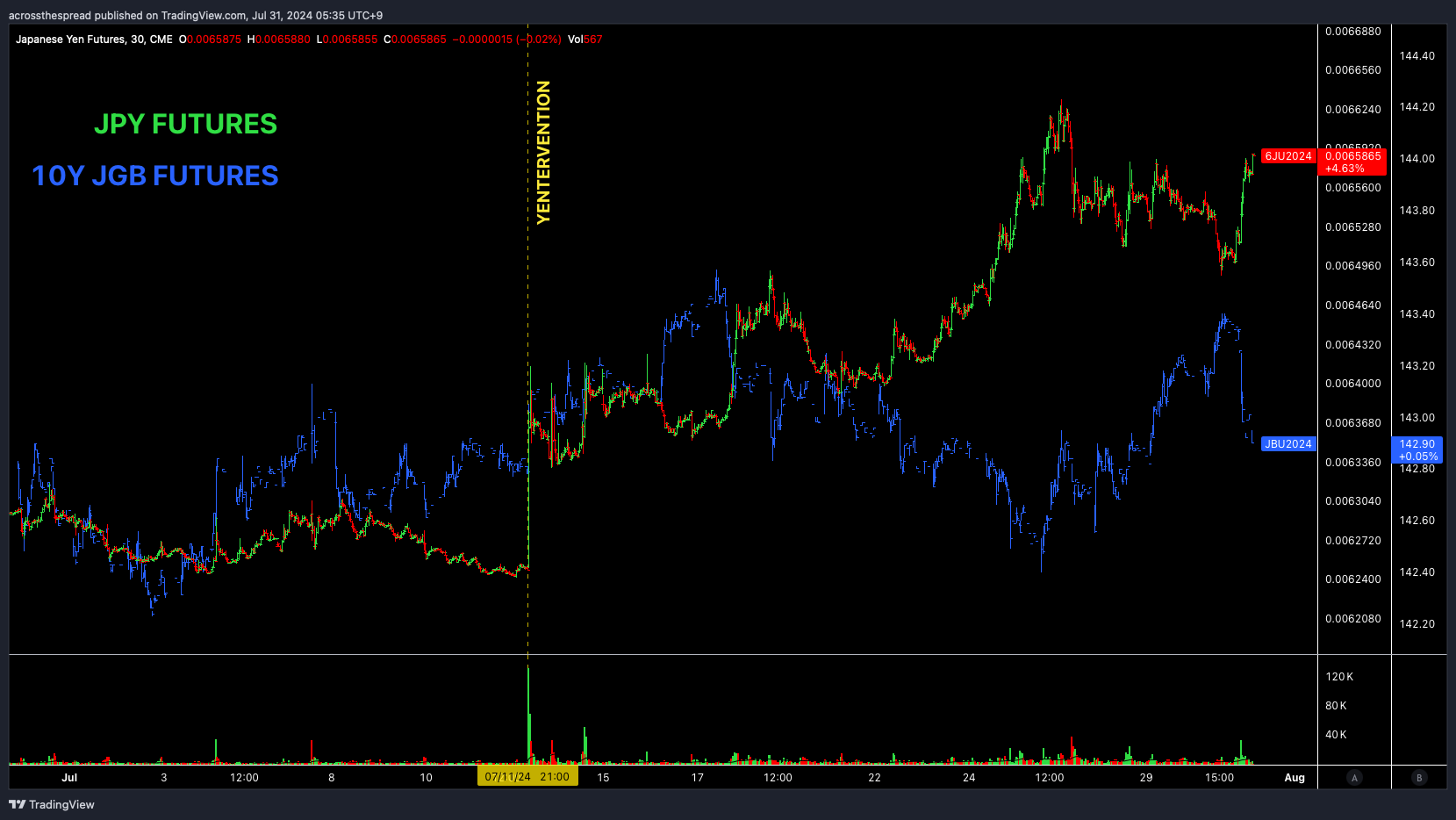

What we do see however, is a sharp market move for JPY strength shortly after 12AM midnight in Japan.

And we also saw a sharp sell off in JGB futures at the same time - minutes after midnight:

But none of those carbon copy "BOJ consider hike to 25bps” articles came out at or around that time.

However, this did -

12AM midnight:

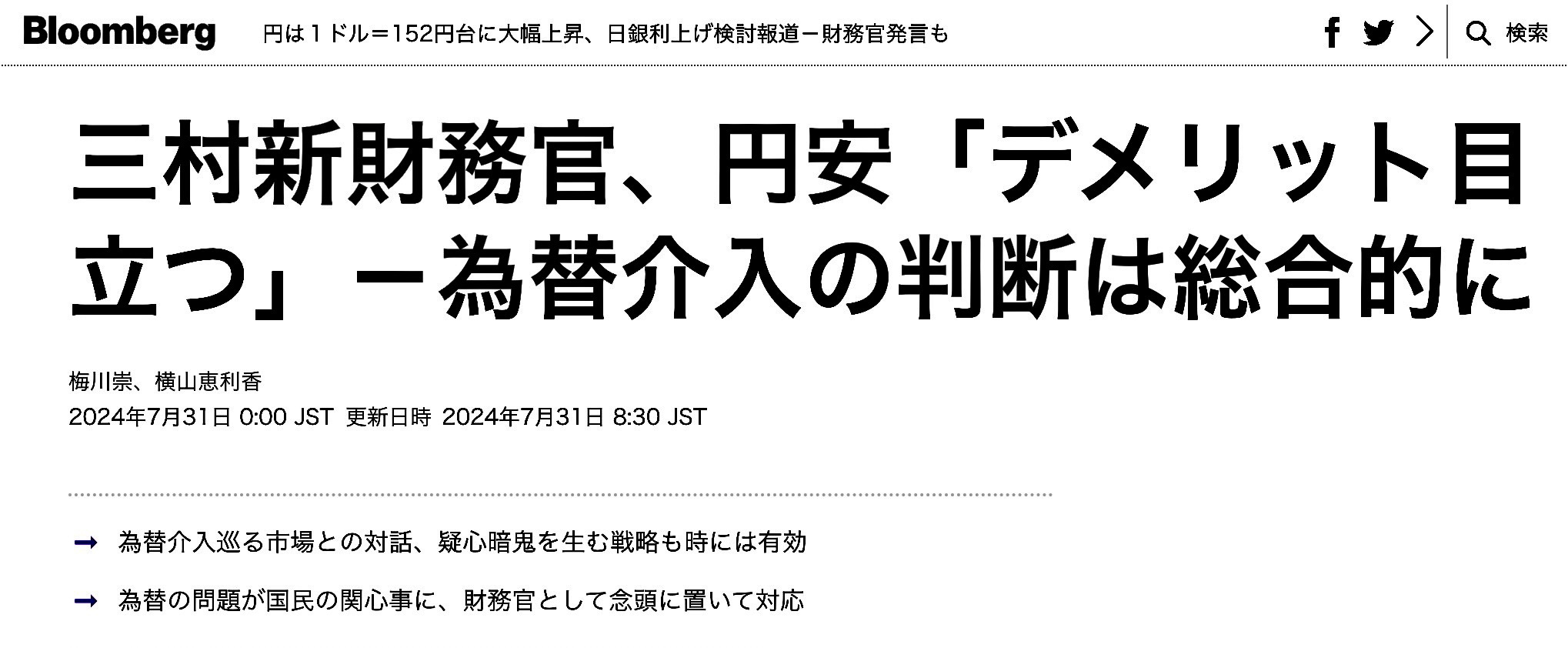

Masato Kanda, who let the yentervention genie-out-of-bottle in 2022 that Japan will never be able to shake off, and thus, the guy who I probably have publicly skewered the most among the many in Japan policy, is no longer the Ministry of Finance Vice Minister of FX Meddling as of midnight, as Atsushi Mimura takes over.

And Bloomberg dropped the interview at 12AM midnight in which the main quote and headline takeaway of the new guy was…

“While the recent depreciation of the yen has both advantages and disadvantages, the demerits are becoming more noticeable,” said Atsushi Mimura, vice finance minister for international affairs in a Bloomberg interview Monday.

Not really too profound, but I suppose that if there were assumptions of any departure from… the "conventional norms” of (extremely unconventional) yenterventionism may be priced out. And that in itself is not as market significant as showing how little impact (via skepticism, or not caring/priced in) a BOJ rate hike rumor is.

Instead, the following from this Bloomberg interview article the most important and revealing passage of the Bloomberg interview article

Mimura also hinted he may continue his predecessor’s strategy of keeping investors guessing over when Japan has stepped into markets to prop up the yen.

Japan said it spent a record ¥9.8 trillion ($63 billion) in the reporting month of May on currency intervention, about a month after two suspected moves. Since then Tokyo is believed to have stepped into the market another two times, with official disclosure of the amount spent expected later Wednesday after weeks of no comment.

“Predictability is important in some cases, while in others it makes sense to be unpredictable,” Mimura said.

Much in the way that communication “isn’t pre-set among family, friends and colleagues,” talking to the market is “something you think about in that specific situation. Ultimately that’s it,” he said.

Bloomberg: Japan’s New FX Chief Says Weak Yen Doing More Harm Than Good for Economy

And that, my friends, is what I'm talking about regarding these mini, stealth yenterventions, attacking with momentum, rather than smacking a runway USDJPY the opposite direction. In fact, this general concept is something I had been talking about since exactly one year ago, July 2023 when BOJ adopted the strategy of “flexible optionality” - which comes at the expense of us market participants’ confusion and ambiguity. Or, what I have been calling “YCC-C” - Yield Curve Control-Control, in attempt to regain control of the market out of the hands of us market participants with purposeful ambiguity of when, how, and how much to intervene (be it JGBs or JPY).

So, that is what we are up against - I have a feeling that this guy is far more market savvy than Kanda (not a high bar).

Final Thoughts heading into BOJ:

Here is the "Nikkei has learned” media leak that actually matters most:

I think BOJ's JGB tapering will disappoint - or rather, that BOJ thinks that markets will be disappointed (regardless of whether or not they are).

Consensus is for trimming JGB purchases from current (approximate) 6 trillion yen per month, to half - 3 trillion per month, over the next 2 years. Also note that the approximate 6 trillion yen figure is the over/under for QE/QT - given the projected JGB held to maturity balance sheet run-off, net of buying. Below 6 trillion per month would net-shrink the balance sheet as more JGBs mature than they are buying.

The above article suggests they really don't have much wiggle room, at least not enough to really move the psychological needle on “QT-ing.”

I think that should a simultaneous rate hike occur with today's QT, it will be a hedge against disappointment and market consequences of a weak yen move.

I think that under new guy at MOF, and under MOF's new approach of hitting the market (USDJPY) down WITH momentum in smaller, under the radar increments, rather than large $30bn per clip smacks - BOJ (who is more currency minded at this moment than JGB yield minded) may also adopt this work-with-momentum dual rate hike and QT. Or rather - I'm split on that, but if they were to go that dual route, that would be the reasonable justification as to why.

Other things to note that are different this time:

BOJ's monthly schedule of JGB purchasing is supposed to be released at 5pm today, as per the last business day of every month. 5pm is a few minutes after Governor Ueda's press conference.

So, whatever they release and announce for the policy statement, and whatever Gov Ueda says at the 3:30PM press conference - there is still a 5pm explicit policy release (unless they release it along with the policy statement around noon). And it may very well be that they have different versions ready to release, to be decided on last minute based on market reaction. Or not- but either way, be aware that there are THREE policy events today: policy statement release (around noon), Gov Ueda press conference (3:30pm start), and the August JGB buying schedule (5pm).

Lastly - note that JGB yields and JPY have returned to a JGB yield up → JPY stronger relationship, that had been completely opposite behavior from April yentervention - just a heads up for market behavior relationships.

Will follow up.

Weston