JGB 10Y Yields Rise Above Key 1% Level, Still No JPY Strength

Market Update: Japan continues to trade like an emerging market - as JGBs and JPY simultaneously sell off against market conventions. What in the hell does BOJ and/or MOF do now?

Japan financial authorities are facing a big problem in their war with markets - the fundamentals of market dynamics aren’t behaving the way they’re “supposed to” be with regards to JPY strength (or lack thereof).

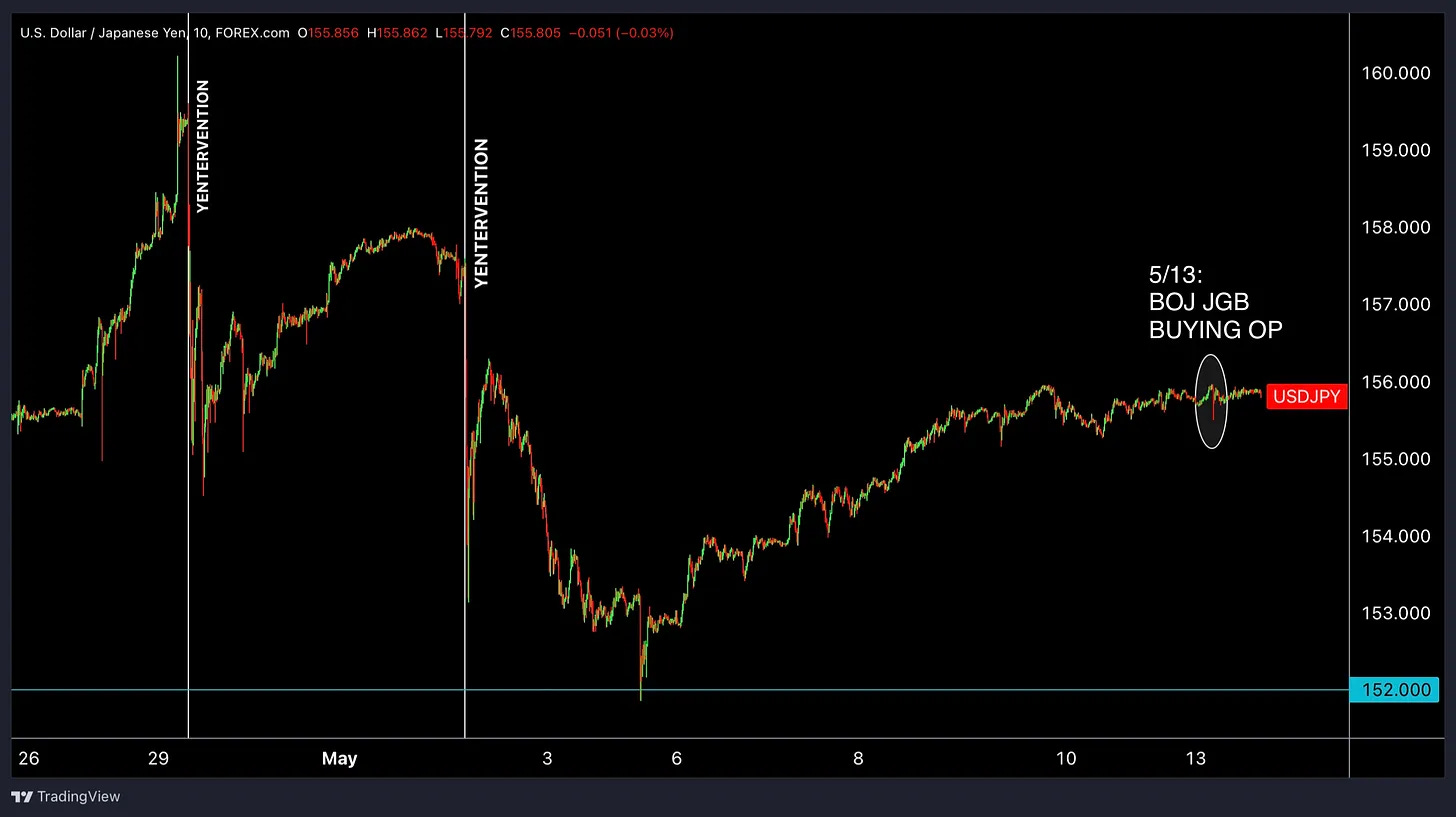

Ministry of Finance’s direct yentervention didn’t do much in reversing JPY’s sharp decline to multi-decade lows.

And now, the Bank of Japan “allowing” for JGB yields to rise to previously “unacceptable” (explicitly capped under YCC) levels, even as US yields decline and yield spreads narrow, isn’t helping JPY regain footing either - regardless of whether BOJ’s higher yield tolerance has anything to do with currency-related matters or not.

Last week, I flagged JGB yields - which were not only breaking out at every tenor across the entire yield curve with 10Y JGB yields closing in on the critical 1% level that was breached today - but I also flagged that JGBs and JPY were trading directionally in-line with one another (JGB yields up, USDJPY up), as opposed to inverse.

In other words, Japan is currently trading like an emerging market.

And there is seemingly nothing that Japan officials, neither MOF for currency or BOJ for JGBs, can do about it - because markets are not behaving how they’re “supposed to” be - US yields and U.S.-JGB yield spreads are down, yet USDJPY up.

In terms of green and red blinking ticker market dynamics - yentervention week has really fucked things up.

And there are broad market implications as a result of capital flight from Japan- positive for U.S. and non-Japan DM equities (EM as well, namely India and China), gold, USTs and more.

Following up from:

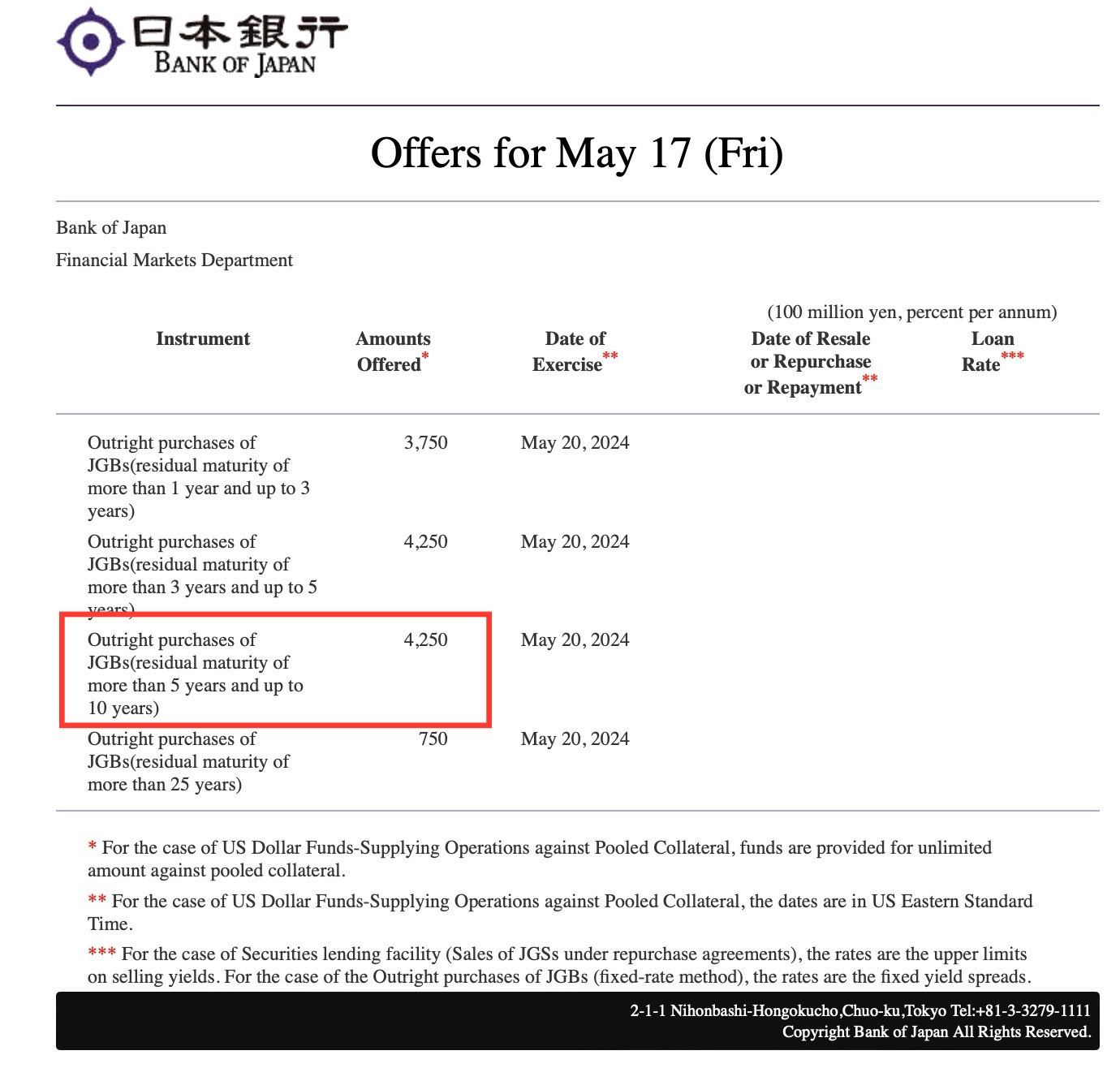

Friday May 17th:

BOJ kept its regularly scheduled JGB buying operation unchanged from the reduced amount of buying in the 5-10Y tenors that it had suddenly cut on Monday May 13th, when BOJ bought -¥50 billion less in 5-10Y JGBs that they had bought the last time 5-10Y JGBs were purchased by BOJ on 4/24: ¥425 billion worth of 5-10Y JGBs vs ¥475 billion previous. - which caused this current leg of accelerated JGB yield breakouts underway.

USDJPY jumped when the above details of the day’s BOJ buying operation was released on Friday at 10:10AM.

The magnitude of the move in JPY market reaction itself isn’t anything crazy (hard to beat “crazy” when we just saw USDJPY trade in a range from 155 → 160 → 151-handle within a week), but nonetheless a decisive directional move higher (JPY lower), and maintaining since.

Moreover, it shows a JPY market that is apparently behaving/reacting to Bank of Japan’s current JGB activity as follows:

If BOJ allows for higher JGB yields via reducing the amount of JGBs they’re buying in their regular operations - JPY does nothing (even if US yields are meanwhile falling)

If BOJ does not continue to further incrementally reduce the amount of JGBs they’re buying from operation to operation - JPY falls / USDJPY rises (even if US yields are meanwhile falling).

Or, simply from a purely green and red blinking tickers standpoint…

Keep reading with a 7-day free trial

Subscribe to Across The Spread to keep reading this post and get 7 days of free access to the full post archives.