What BOJ Thinks of Japan Wages and Negative Rates

Japan market commentary: NKY, JPY, JGBs. Negative rates. +BOJ's (Japanese-only release) Wage/Price Report translated to English

Japan is in financial news headlines again, for “all the wrong reasons.”

You’re probably getting headlines from today of Japan wage data coming in “strong,” coupled with BOJ and Japan government officials jawboning a BOJ negative rate exit perhaps as soon as this month’s March policy meeting- and Japan markets are reacting accordingly: NKY down, JGB yields up, JPY strong.

And if so, you're being mis/un-informed, and in more ways than one: as Bank of Japan has been releasing their "policy review” reports spanning the last 25 years of BOJ policy experimentation- an endeavor that Governor Ueda had announced upon his inaugural BOJ meeting. Only thing is - he didn’t bother with English (or non-Japanese) versions of these vital, policy signaling publications - for whatever reason. Which is why I’ve translated to English and attached the latest official BOJ Review at the bottom of this article.

First, let’s run through each market/asset class, and then discuss the state of Japan wages, and how BOJ may be influenced- as these headlines are empty non-explanations in need of a sliver of substance.

NKY

I will follow up comment on the NKY and equity markets after SQ (“special quotation” - March quarterly index futures and options expiry) tomorrow. Just remember, this is exactly why I had flagged NKY index futures and options last trade date (today) and the NKY 40,000 level in my prior article warning of this very nonsense as such:

NKY March futures are currently selling off -2% as I write this, and NKY March 40k calls are quickly becoming worthless (after having just surged).

Either way, this is not an equity market “reacting to BOJ potentially removing negative rates” - as if that’s an entirely new concept that was just realized by markets and interrupted the +20% year to date NKY blast off. Swap traders have a BOJ negative rate exit by April at 80% priced in.

People are.. aware.. about BOJ negative rate fiddling.

JPY

…is strengthening - USDJPY is falling, now breaking into the 147 handle, -1% on the day.

To reiterate the NKY commentary above - this too is not some market reaction to “end of BOJ negative rates coming to a theater near you” just now getting realized in FX markets. In fact, as it relates to USDJPY, this isn't a “yields higher” (via BOJ rate lift) story - its the contrary. USDJPY is simply "catching down” to falling 10Y UST yields.

Note that in early Feb, USDJPY was similarly led down by yields / yield spreads directionally, but USDJPY had also resisted from going the full magnitude of the way down - which shows that the yen selling pressure (or buying the USDJPY dip) was formidable.

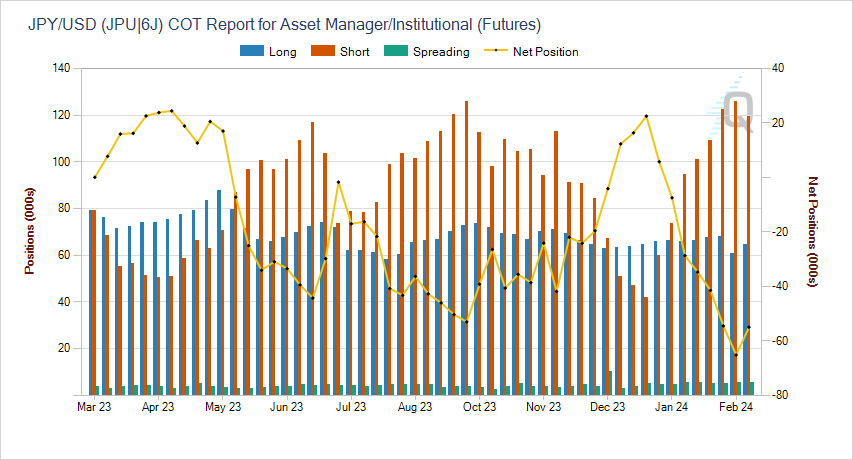

And we can see this early Feb “resisting” of JPY strength was an effort by hedge funds, who nearly tripled the size of their net short JPY futures from end of January, to now being positioned most short JPY futures in years.

Which is actually unsettling, if not alarming - as the 150-ish level is JPY's yentervention floor, and that's where levered funds have crowded into - the lows.

That said, the levered funds category is ceding its share of the overall JPY futures positioning complex, starting the year at 33% and currently at 25% of total open interest.

On the other hand, Asset Managers continue to account for the largest share of JPY open interest at 33% latest reading - and while they too ramped up their net short JPY positions (albeit less erratically than the hedge funds did), it seems these (slightly) bigger fish may actually now be turning towards closing their yen shorts.

One week doesn't make a trend, but if that's the direction of travel anyway, and markets get a shove in that very direction, it can fast-forward the move, and potentially violently so.

Again, current market is -1% down on USDJPY for the day, and off its ceiling highs. No big deal - BUT, considering that we are also just a few hours from ECB (even with consensus expectations of a hold), it can be eyebrow raising to see such trading activity NOW, ahead of a major central bank, of all times. Unlikely that someone is actually trading like that- seems like forced exiting underway, in a crowded market at it's upper range. Something to keep an eye on.

And should JPY make a sharp volatile move, lets not knee-jerk go to "BOJ negative rate related.” (Also, I'm not talking to you if you’re reading this- I'm "talking to” fin media regurgitation machine.)

JGBs

Step aside, long-end - it’s all about the 2Y JGB yield. Why? Because for once, it’s not about the 10Y yield and YCC - it’s currently all about what BOJ will/won’t do with its negative front-end policy rate (or rather, when). And therefore, the shorter-dated 2Y JGB yield is in focus, and for good reason.

10Y JGB yield chart below over the past year - I’ve marked key moments: the March ‘23 Kuroda finale BOJ unchanged + March JGB futures expiry + global sovereign yield collapse lows, the July BOJ YCC 50bps → 1% shock, and the day-after Halloween BOJ in which they vanished the YCC ceiling, only to step in to buy JGBs in an unscheduled operation the very next day, which put the floor under JGBs / cap on yields and triggered a massive short cover.

And currently, 10Y JGB yields have been floating around in the non-threatening 70bp handle - far enough away from a no-longer-explicit 1% upper bound ceiling. Nothing to see here.

Same goes for 30Y JGB yields below.

Same November 1st top, and currently meandering around aimlessly, but not alarmingly.

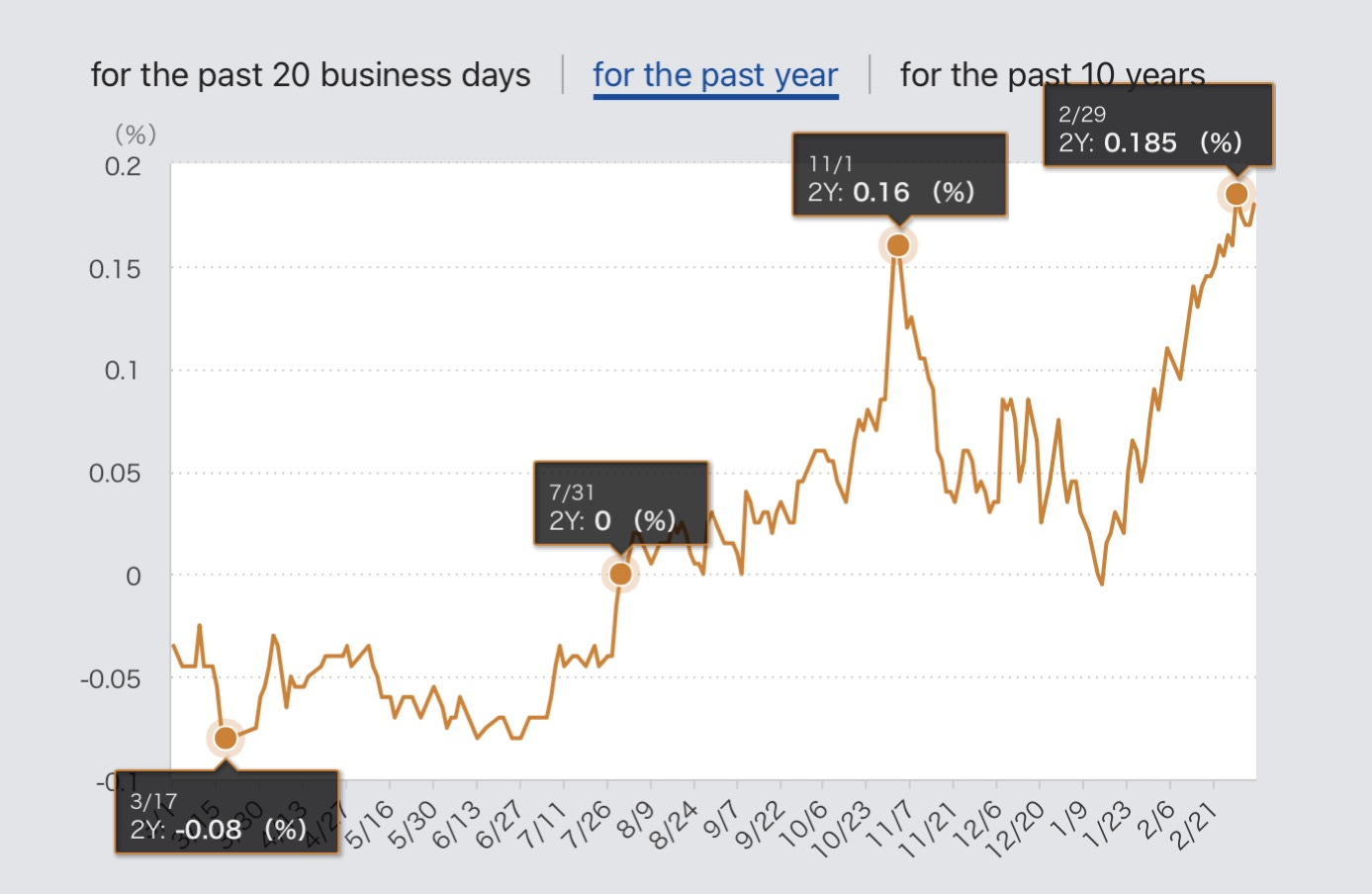

Now take a look at the 2Y JGB yield. We’ve been holding above the Nov 1 highs for about a month now.

In fact, 2Y JGB yields have actually broken out to 13-year highs - meaning 2Y JGBs are currently yielding far above the Jan’16 pre-negative policy rate levels. In fact, they’re now higher than at any point during the decade of Kurodanomics.

Mind you, 2Y JGBs were actually yielding in negative territory less than 2 months ago in mid January ‘24 - but have now shot up to a basis point shy of 0.2%. That's a pretty extreme move AND yield level. Certainly seems to have way overshot for even the most "hawkish” of BOJ scenarios.

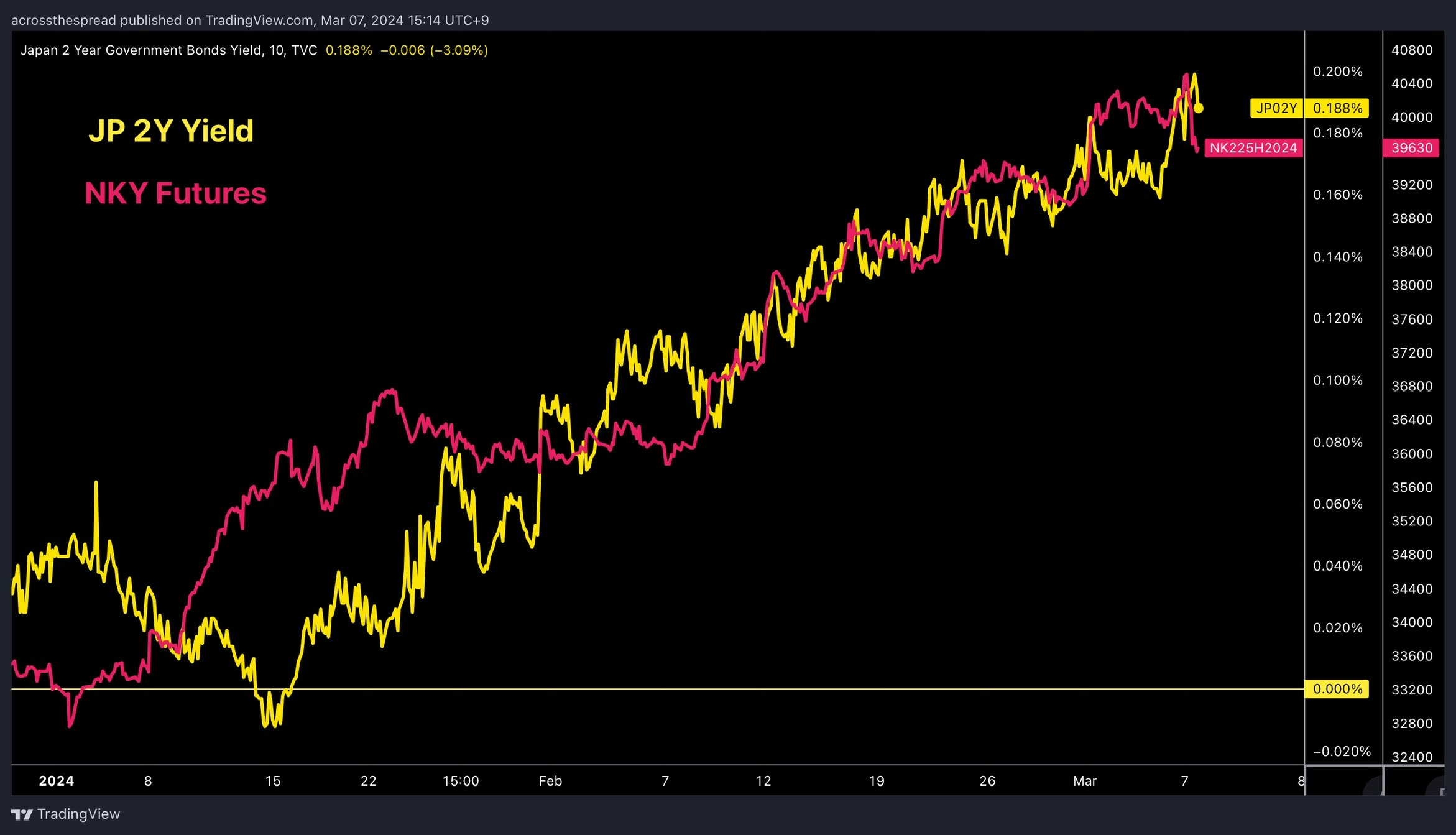

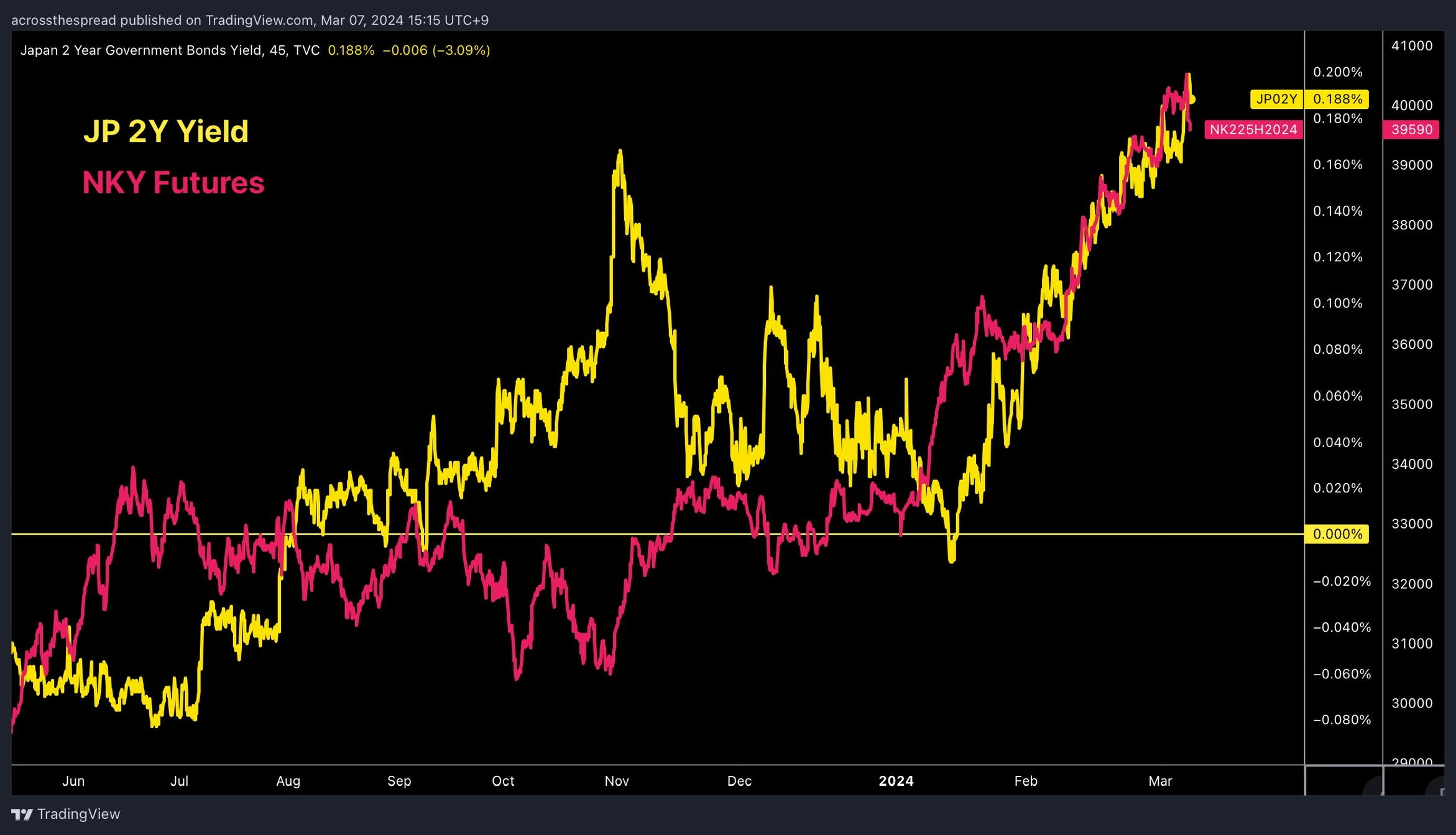

I then also noticed this: 2Y JGB yields and NKY:

No, this isn't anywhere near as clean with any other JGB tenor other than 2's. And no, this is definitely not a “usual occurrence.”

If anything, NKY and 2Y yields are inversely correlated over what looks like 20-40 day periods during the great 2023 NKY upside breakout (and absent the great 2024 NKY upside breakout).

This NKY & 2Y JGB yields parallel move is something I'm still trying to think through (if anyone has thoughts, please feel free to share - publicly or privately). It could very well be nothing. But I'm thinking something along the lines of- foreigners (who are actually predominant holders of short dated JGBs) using collateral, and tie-in with Japan equities exposure somehow. Or - to the subscriber who is the cross currency basis swap trader who very kindly reached out to me (you know who you are) do you CCY basis swap traders ever use proceeds for funding long risk assets / equity derivatives or something? Anyone else have an answer or a guess? As you can see, I yet to have an idea as to why 2Y JGB yields & NKY match up- just an observation at best for now.

Bank of Japan Negative Rates View

I personally don’t have a conviction view on Bank of Japan’s negative rate policy at the moment, nor have I ever really had one (and I don’t really understand how anyone can/does as much as they do). But here is my only commentary and view on the matter.

Bank of Japan will lift the policy rate from -0.1% current, to 0%.

That’s it.

Extremely boring, I know - though I actually do have reasoning behind it. But first- this is somehow an out-of-consensus view. And its not/never from me searching to be “anti-consensus” - its what I genuinely think, and that happens to not be in-line with the majority.

It seems that by and large, all calls regarding the BOJ negative rate is for it to go positive- everyone skips over 0%. My view is that the BOJ will “live at zero.” I think getting out of negative is the desire and aim - not the raising of rates.

0% is as neutral with max optionally as it can be, with the least damage done, AND removing the damage FROM.

I see BOJ “hiking” back to the zero bound, so that banks can finally stop complaining (rightfully so), but still having extremely accommodative interest rates- free. Zero. Nothing.

And I have no real timeline - probably likely sooner than later (within the next 1 to 3 meetings) simply based on BOJ's public messaging behavior, but no way to pinpoint.

(I actually do have far more in depth thoughts on this matter which I will lay out in another article- mostly what potential market reactions may come, which is absent from the broader dialogue - but I realized that I had never actually given my negative rate view. So here it is for now.)

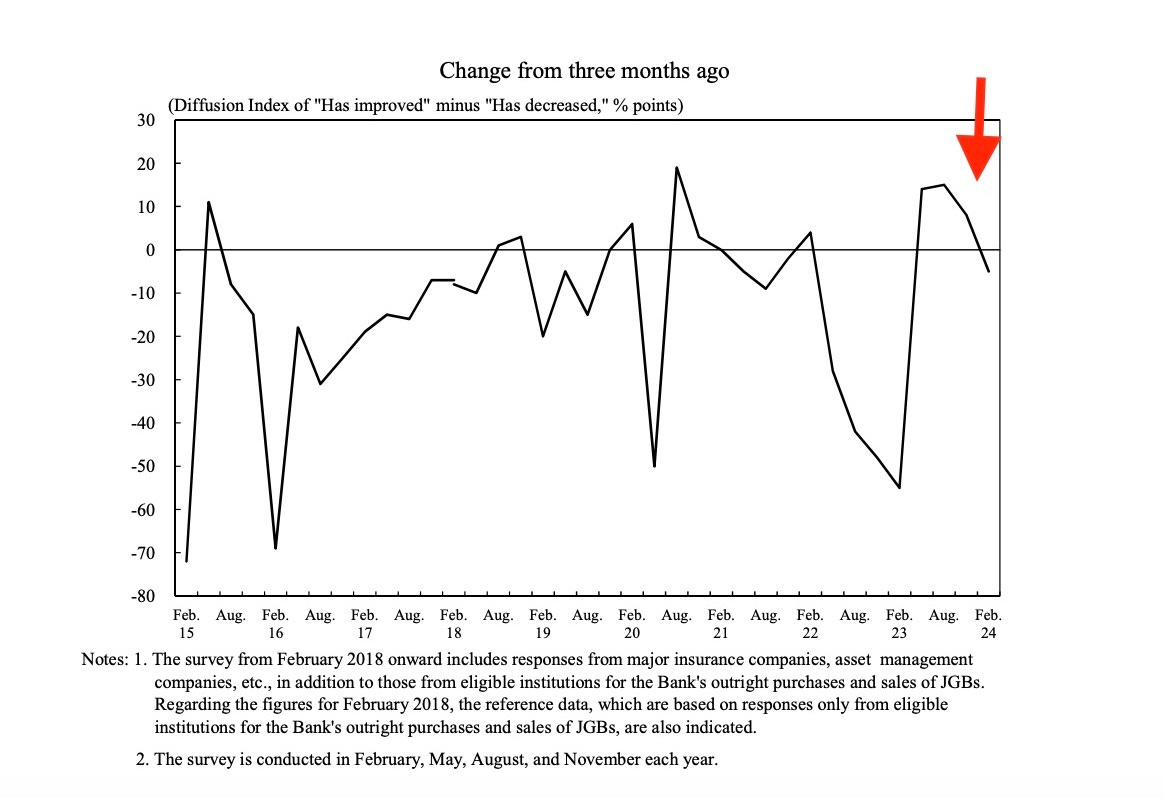

But ultimately, what will give the green or red light to tinker with the BOJ policy rate will be market conditions. And when looking at the latest BOJ Bond Market Survey (which is all one ever needed when looking at prior YCC changes/maintains): bad news (for those expecting policy change) - the Degree of Bond Market Functioning (period-over-period delta) has dipped back into negative (this is a diffusion index ±0, kind of like how PMI readings work- above/sub 50)

👆THIS (and measures like this of market stability) is what overrules anything else - labor cash wages, CPI, political pressure, whatever secondary measure it may be - this can put a halt to the whole thing.

Bank of Japan Bond Market Survey (February 2024)

Japan Wages and BOJ

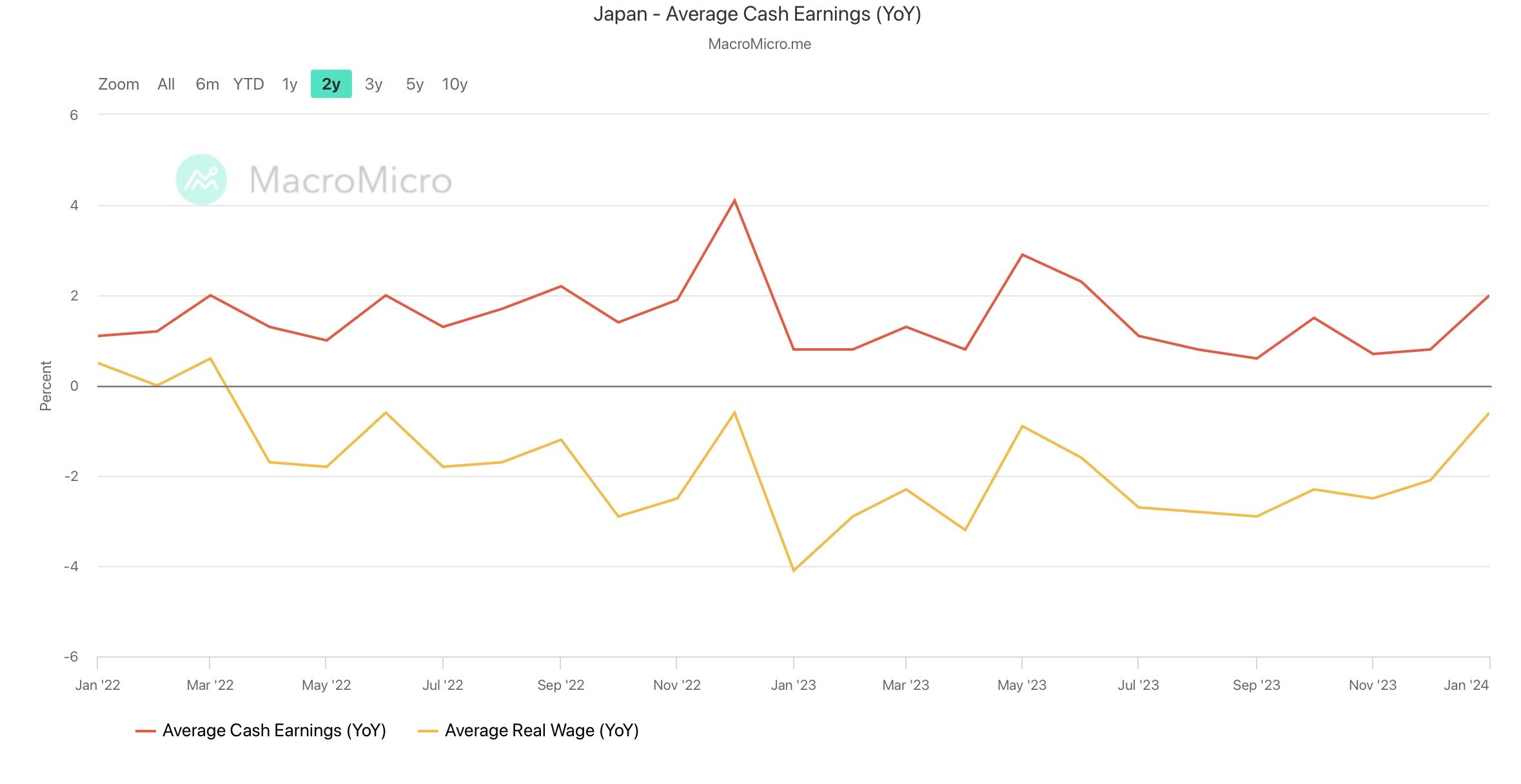

Nominal wages are at 2% - hooray. Real wages are still negative for the 20-something consecutive month. And while yes, its on an uptrend, real wages negative doesn't scream "BOJ- get out of negative rates ASAP!” In fact, to get a rise in both nominal and real wages in Japan, and then to have that trend higher in a stable manner - that’s basically Japan's socioeconomic equivalent of 2 pandas mating. You don't want to disturb such a rare and much needed miracle, lest the species face extinction. Ueda has said on a few occasions that the risk of running the economy (price increases) hot far outweighs pulling the plug too early.

With all that said, the above data of Japan average wages from earlier today absolutely does not matter- because next week on 3/15 is when we will get the first round of the very closely watched Shunto spring wage negotiations - deeming this backwards looking Average Cash Earnings reading useless.

This is why I am saying that today's financial media theme of “Japan wage data = BOJ negative rates coming = NKY, JPY markets reacting” = nonsense. Markets and asset classes are moving for their own idiosyncratic reasons - and not “in response” to BOJ negative rates coming.

Now- if you really do care to know what BOJ “thinks” about wage inflation vs CPI…

Bank of Japan Policy Review Translated to English (because its exclusively in Japanese for some reason)

In April 2023 after decade of radical monetary policy experimentation under Governor Kuroda, a brand new Governor Ueda took the helm at the Bank of Japan for his first policy meeting. And, as the Nikkei had pre-leaked out to markets on the MORNING OF the April BOJ policy announcement (great starting impression, Ueda), while there was no change to existing legacy-Kuroda policy, the quiet college professor turned most powerful man in Japan announced that the Bank of Japan will embark on a rigorous self-reflection spanning a quarter-century of monetary Walter-White-ing, and periodically publish their findings to the public. This was to be done alongside live policy tinkering (like a coach reviewing the game tape in the 2nd inning of that very game), thereby making these little report-drops as potential tools themselves to be used to influence real-time or imminent policy perceptions and even alter market positioning, no different from when they get Nikkei news to press-test policy on their behalf.

Bank of Japan Statement on Monetary Policy April 28, 2023

Since the late 1990s, when Japan's economy fell into deflation, achieving price stability has been a challenge for a long period of 25 years. During this period, the Bank has implemented various monetary easing measures. These measures have interacted with and influenced wide areas of Japan's economic activity, prices, and financial sector. In light of this, the Bank has decided to conduct a broad-perspective review of monetary policy, with a planned time frame of around one to one and a half years.

Cool- whatever, do your little self-reviews.

But then I noticed that these were actually starting to come out on the BOJ website- but only in Japanese, on the BOJ Japanese website. What the fuck is that all about? I honestly don't know, nor do I care why these are only available in Japanese - I just care that they are, and are not available in English or any other language.

Bank of Japan - you are a major G5 central bank, and like it or not, are a vital organ to the global economy - so get your act together and communicate to international markets, and not exclusively to your “jurisdiction.”

Its bad enough that Governor Ueda's press conference transcripts are only released in Japanese (the Japanese are the ones that can re-watch the video of you fumbling your answers with your shaky voice- its the rest of the non-Japanese speaking world is who is in need of transcripts, idiot). But seriously, you're also going to not have English/non-Japanese versions of your seminal policy reviews?

And its not like they don't have the ability to translate either - see any BOJ policy statement, or any of their 50-page research reports. So, for whatever reason, this is being done on purpose. This is beneath even PBOC standards - just horrendously unacceptable.

There have only been two such official BOJ policy review reports published so far - the first one I don't even care to remember what it was on. The second official Bank of Japan Review is on the topic of the relationship between Japan's wages and consumer prices. Its 7 pages long, and looks like this:

So - I took this "confidential” document and dropped it into an auto-translator, then went back and tried to clean up / smooth out the oddities, then formatted the English text and charts with English labels to more or less look structurally like the original Japanese one. This was a massive pain in the ass to do - and I personally don't even get any useful value out of such reports (because I'm a green and red blinking tickers markets-guy, not an “economist”), but I know some of you actually might care to see what they have to say - policy propaganda or otherwise. Maybe the fact that they're not even bothering with English versions shows how much of a hollow prop these things are - and they're just saving us from nonsense. But I've noticed a significant culture change from the Kuroda to Ueda regime, and this latest sneaky non-level playing field (as I took it) really pissed me off - so that was my real impetus.

One of our paid subscribers recently asked me about the January BOJ press conference, so I auto-translated/very quick-skimmed the transcript to English - you can find that below too if you wish (note that whenever you see a reporter saying "the president” - that's them directly addressing Governor Ueda).

If you find these (VERY IMPERFECT) translated documents (or ATTEMPTS at doing so) to be genuinely useful, let me know.

Either way, just know that none of this is to be relied on for any sort of accuracy.

BANK OF JAPAN REVIEW: Recent Developments in the Relationship Between Wages and Prices

Executive Summary

Many of the items that make up the CPI are currently affected by substantial fluctuations in existing import prices. Therefore, it is not easy to identify the upward pressure on prices that originates from the wage-price relationship. In this paper, we attempted to quantitatively assess the extent to which the wage-price interlinkage is at work, using multiple approaches. Analysis based on the

Keep reading with a 7-day free trial

Subscribe to Across The Spread to keep reading this post and get 7 days of free access to the full post archives.