JGBs Flash A New Type Of Warning Signal For Global Bond Markets

JGBs Flash A New Type Of Warning Signal For Global Bond Markets

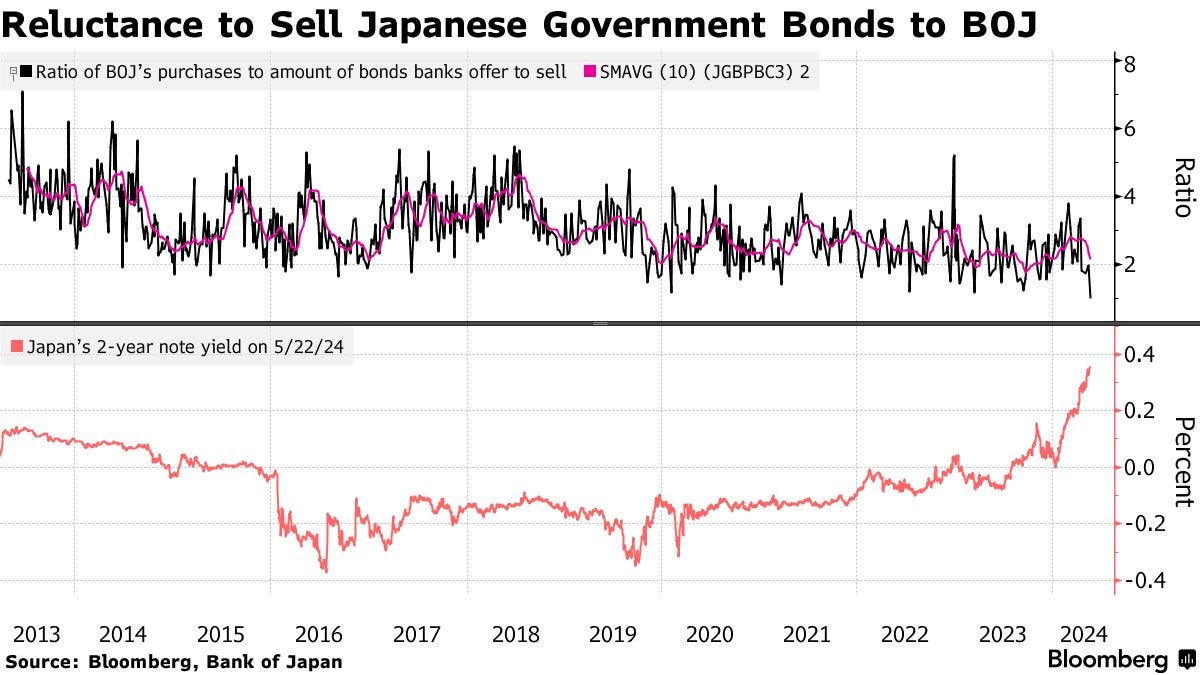

For the first time, Bank of Japan was not able to buy as many JGBs as offered to markets. This is concerning - here is why.

🔹Markets show a first-time ever potential “self-imposed” cap on JGB yields by selling less JGBs than BOJ was offering to buy, and thereby, revealing the only force left to effectively stop JPY downside.

🔹BOJ’s inability to buy as many JGBs as it had always assumed it could is far more significant than realized - as it signals a critical reminder to global DM sovereign bond markets that trading liquidity and functionality remains structurally damaged, and the same underlying problems behind the Sept-Oct’22 UK Gilt blowup and the March’23 global rate volatility bomb still remain.

🔹Examples of the JGB market dysfunction and insanity, and how BOJ screwed JGB futures shorts at the expense of market functionality

Following up from yesterday’s note flagging BOJ’s regular JGB buying op held earlier today.

A very interesting and historic occurrence, if not a concerning signal, and even a potential turn of events in markets is happening.

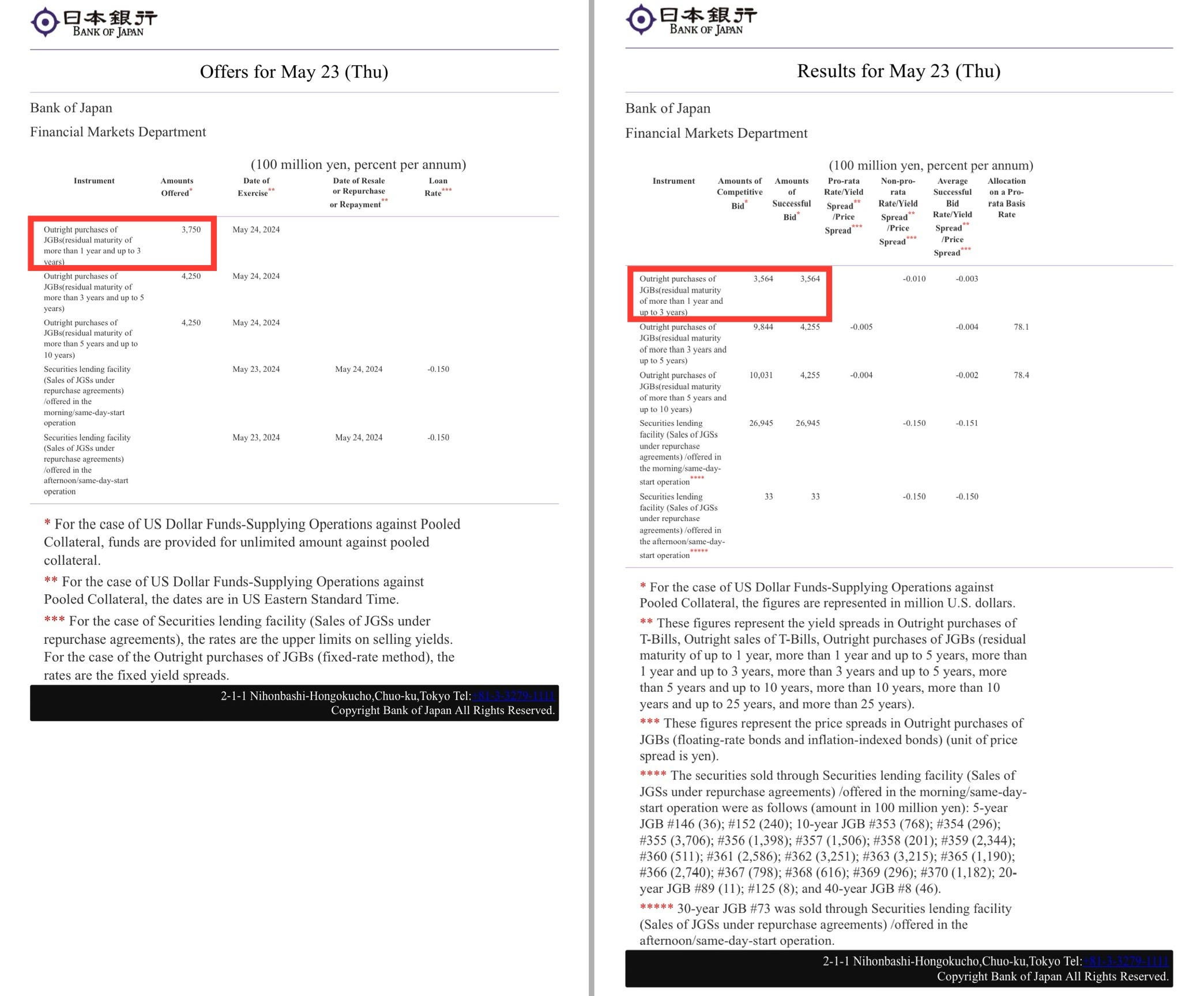

Results from today’s regular scheduled Bank of Japan JGB buying operation targeting 1-3Y, 3-5Y and 5-10Y JGBs:

BOJ kept the amount JGBs it was offering to buy unchanged - with the focus here being on the ¥425bn for the 5-10Y section of the curve that had been reduced last Monday sending the entire JGB yield curve to break out higher, but that ¥425bn offer to buy 5-10Ys was maintained for now 2nd operation since.

HOWEVER - on the FRONT end 1-3Y part of the JGB buying operation, BOJ’s offer to buy ¥375bn was met with WEAKER take-up from investors to SELL that amount to BOJ, where only ¥356.4bn of 1-3Y JGBs was actually sold to BOJ.

This was the first shortfall of BOJ offering to buy more JGBs than market participants’ willingness to sell to BOJ since the start of this Kurodanomics massive JGB acquiring era in 2013 by regular open market operations.

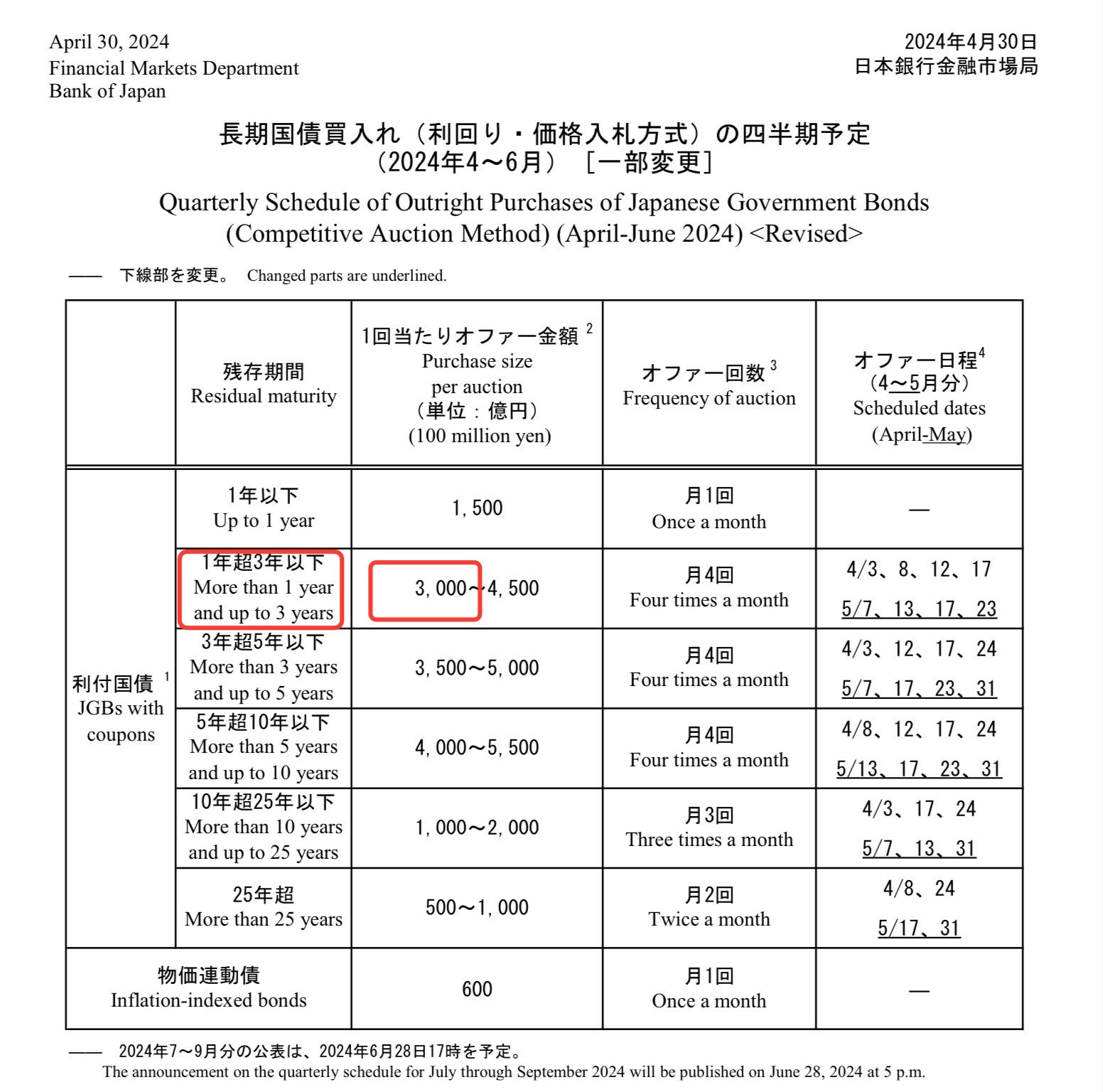

(In a recent note, I showed a step-by-step of how to navigate BOJ’s website for real-time market operation announcements and results - above, you can see the BOJ’s 10:10am published offer amount for the day + the subsequent results of the JGB buying op below, and I’ve boxed in red the relevant figures for how to read these daily releases).

Market Reaction:

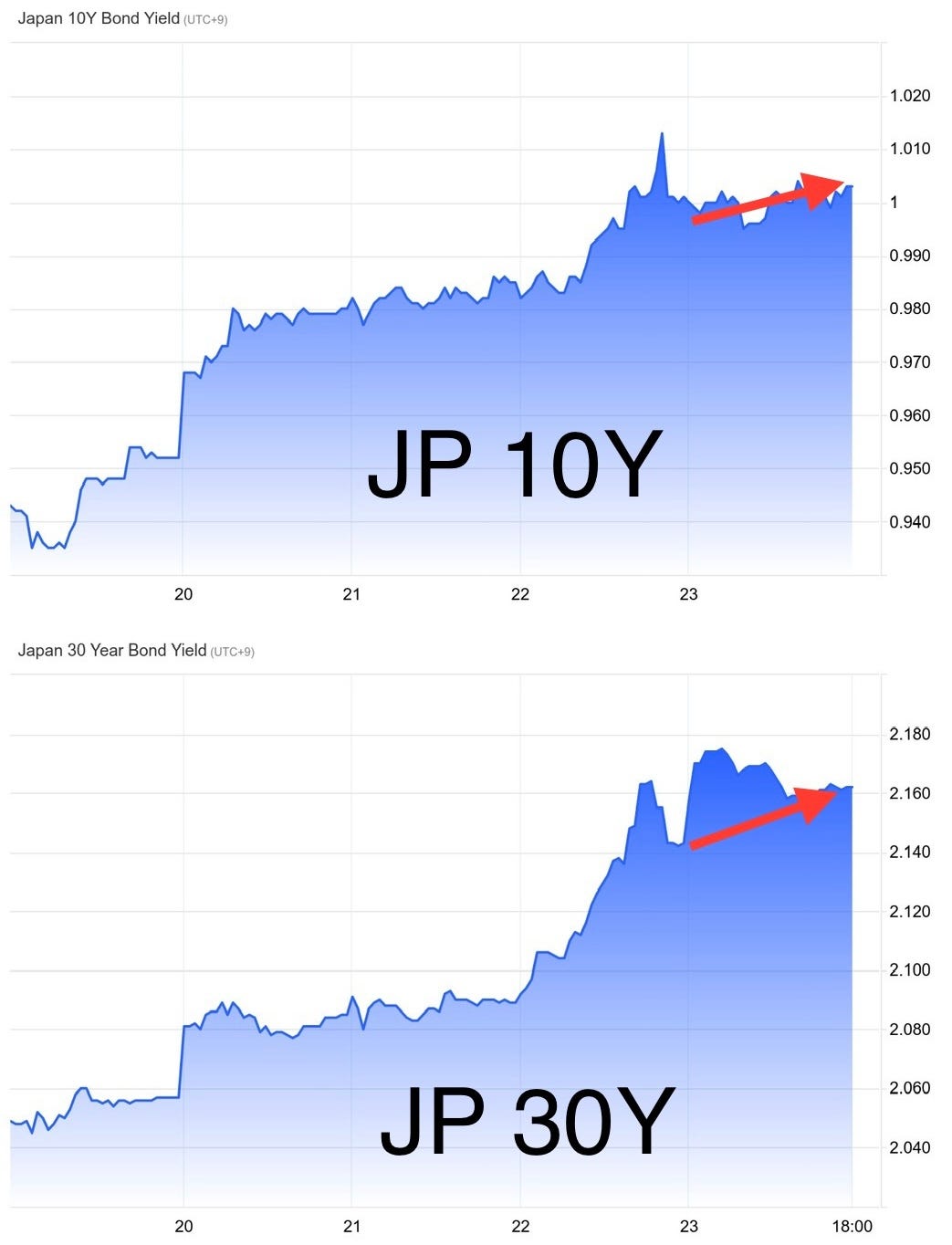

As a result of this rather historic “no thanks” by markets to BOJ’s full sized buying offer - JGB yields on the front end all the way up to sub-10Y maturities fell on the day, halting the relentless surge higher that had been underway preceding.

BUT, yields from 10Y and longer ended the day higher, albeit off their respective highs of the day.

June’24 10Y JGB Futures were overall higher for the day - very active in choppy price action and heightened volume for the AM session. Note the 10:10AM move downward on volume upon the release of another unchanged quantity buying op, and then the move higher thereafter as results of the operation itself subsequently came out.

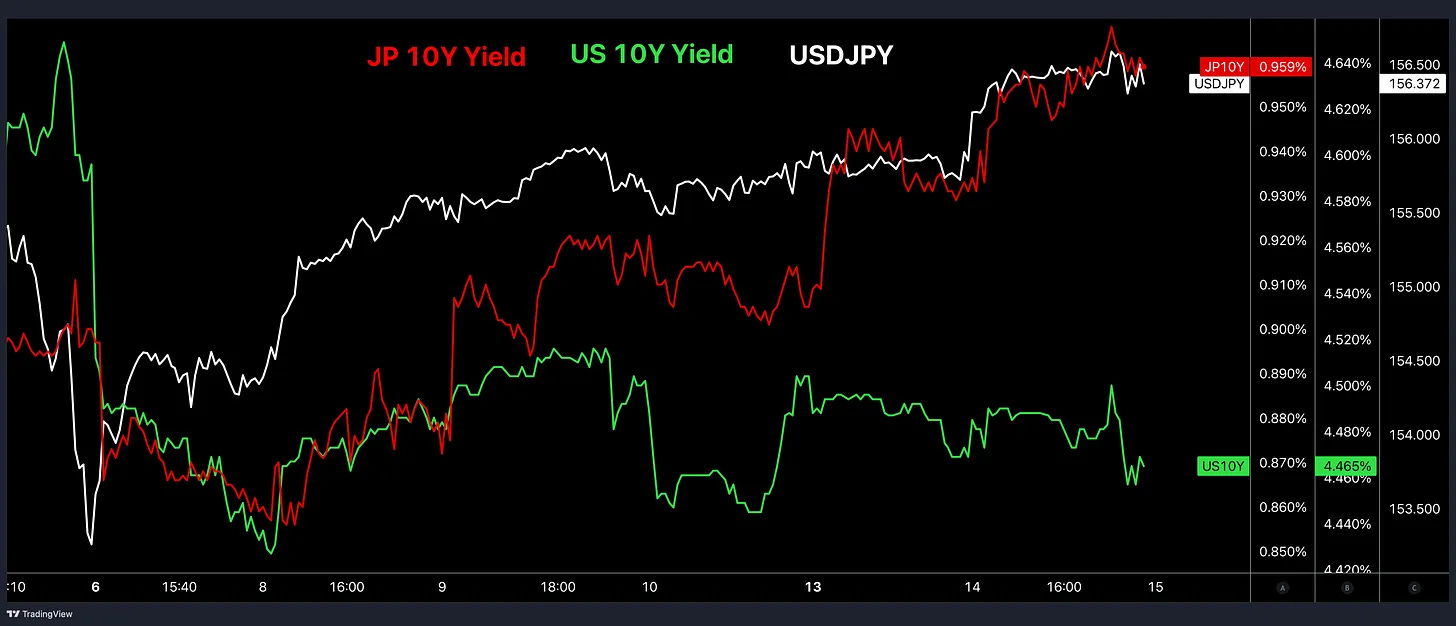

As for JPY - the knee jerk (algo) reaction at 10:10AM was a quick spike in USDJPY to almost hit 157 (>156.90) as the BOJ offer to buy amount was unchanged. However - that marked top tick on USDJPY for the Tokyo trading session, again - as it was revealed that market participants sold less than BOJ was offering to buy in 1-3Y JGBs.

Given the JPY market realities-based backdrop I have been laying out, where MOF yenterventions didn’t work to trigger a trend reversal for sustained JPY buying, nor did BOJ buying less JGBs and allowing for yields to surge (even against falling U.S. yields and compressing US-JP yield spreads), because as I’ve been highlighting - the fundamental behavior of markets in Japan is not what consensus assumes: USDJPY follows JGB yields directionally, as Japan trading like an emerging market.

So, in response to my own question from yesterday’s note:

“…what’s it going to take for JPY to strengthen?

Seemingly nothing from the standpoint of Japan officials’ actions. Nor from U.S. / Fed for that matter - after a non hawkish FOMC Powell and lower than expected CPI print.”

My response (to add) is:

Indeed, there is seemingly nothing that Japan officials (MOF & BOJ) can do to strengthen JPY. But MARKET FORCES can do so, if acting organically and without artificial market meddling interventions by top-down policymakers (in neither JPY directly, nor JGBs) - as today shows.

This is right in line with the broader concept that I have been illustrating for the past year and a half about yenterventions that “work” (Oct ‘22) vs those that fail (Sept ‘22) - non-economic, state actors’ market activities are always and only temporary. They “work” if and only when actual market fundamentals/participants’ activities align accordingly. One-sided, overcrowded positioning that is ripe for a market event (top down meddling) to trigger an initial forced position closing, which then bleeds into sustained momentum thereafter.

Furthermore, if sustained, today’s events may reveal which part of the JGB yield curve that the EM-like JPY behavior is responding to, given the bifurcation of shorter dated JGB yields down, longer-dated JGB yields up. But it is way too early to be able to discern, let alone if that dynamic even exists. Still, something now on my radar going forward.

Last and very critical point regarding this not-selling as many JGBs as BOJ is offering to buy in its regular operations phenomenon from today-

Some out there in JGB-land are saying that this first-since ‘13 level of reluctance for investors to sell less JGBs to BOJ than BOJ is offering to buy in its regular open market operations is happening because of the following 2 reasons:

2Y JGBs (or any short dated within the roughly 1-3Y maturity zone) are being held by investors as a carry position.

Expectations for BOJ to further reduce the amount of JGBs it will offer to buy in the next and subsequent regular operations.

These can both be valid potential explanations, but only depending on the context for each - and they may actually be one in the same. Either way, they are critical to explore.

Just to quickly address whats wrong with each.

For the first one - sure, it’s possible (or even extremely highly likely) that investors are holding onto short-dated JGBs, which have lower duration risk, as a carry trade position. Of course they exist out there. In fact, forget the specific carry trade reason - let’s just say there are an infinite combination of motives for existing investors to not sell to BOJ today.

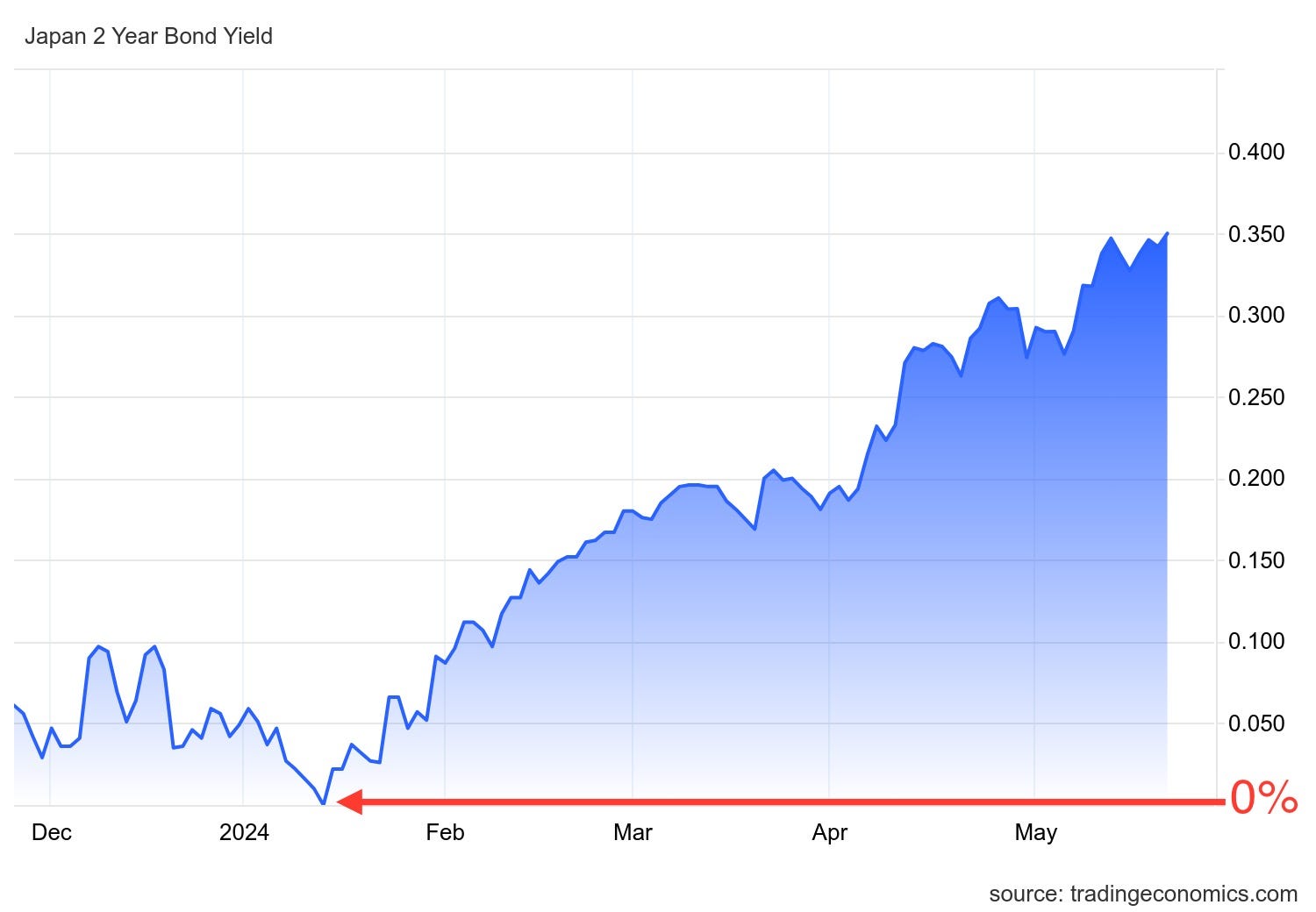

But - let’s also not lose sight of the prevailing market trend either. As I keep mentioning in the past several articles - JGB yields have been surging (JGBs are getting sold down) at an extremely rapid pace this year, particularly at the front end. 2Y JGB yields at one point in Jan 2024 actually traded negative - a sub-zero yield, before going on a one-way blast higher to new multi-decade highs:

Just look at how far and how fast 2Y JGB yields have broken out and have been screaming higher relative to the magnitude of its usual movement in either direction over the last 2 decades:

So - carry trade or otherwise, are people long 2Y JGBs who are unwilling to sell to BOJ out there today? Yep, 100%. And regardless of those holders, are 2Y JGBs getting absolutely crushed at the same time? Clearly, yes. Look at the chart. The market has had no qualms about selling off 2Y JGBs in a near fire sale manner in 2024 - and those holders/reluctant sellers didn’t just show up literally overnight for today.

BUT - perhaps their MARKET PRESENCE DID show up today - and I will get into what I mean by this.

Which brings me to the second point - expectations that BOJ will scale back the amount of JGB buying at the next regularly scheduled buying operation.

Bloomberg published the following article today on this matter - in which they said:

Bloomberg: Bank of Japan Faces Shortage of Sellers in Bond-Buying Operation

“The unexpected outcome looks set to fuel speculation that the central bank will reduce debt purchases more broadly as it winds back monetary stimulus and allows borrowing costs to rise in Japan.

The implication of the shortfall is that there is now a chance that the central may trim purchases at the next operation on May 31, said Shoki Omori, chief desk strategist at Mizuho Securities Co.”

The article includes the following chart:

They are suggesting that due to this first-since 2013 lack of selling has now boosted expectations for further reductions in JGB buying by BOJ’s regular scheduled operations going forward - and I don’t disagree that those expectations have now heightened, as well as my own expectations for that to now happen.

After all- today’s offer to buy ¥375bn in 1-3Y JGBs came in at the lower range of BOJ’s monthly published schedule of ¥300bn ~ ¥450bn. That said, today’s offer is still +¥75bn from the ¥300bn range floor. So, a reduction of say -¥75bn less in JGBs being offered to buy at the next operation would still stay within their stated range.

Reminder - last Monday’s reduction of 5-10Y JGBs was only -¥50bn, and non-consecutive (albeit this was before today’s historic market rejection of BOJ’s full offering amount).

What I will say to potentially counter this narrative is the following.

First - note on the document above that although there is one more JGB buying op scheduled for this month on May 31st, it is not for the 1-3Y tenors - as far as scheduled buying ops are concerned, buying in 1-3Y are done for the month.

So, for those who are calling for an immediate reduction in JGB buying at the next JGB buying op on May 31st (as the Bloomberg article suggests) - I disagree with the premise that it will be a broad-based, duration-agnostic reduction of scheduled JGB purchases, and thus disagree that it will occur at the next scheduled buying op at 10:10AM on May 31st.

Having said that, I DO agree on “May 31st” being the potential catalyst date in the sense that it is the last day of the month, and therefore will have a new monthly JGB buying operation schedule published at 5PM for the month of June - and THERE we may see a lower low-end range for the amount of 1-3Y JGB purchases per operation listed.

I will also say that if indeed there are now expectations by market participants that BOJ will continue to incrementally reduce the amount of JGBs they are offering to buy, then this may very well have the effect of markets capping yields upon themselves (as they’ve done today at the front end of JGB curve). If the expectation is that yields will be higher (prices lower) due to less JGB buying by BOJ, then under the prevailing market conditions of JGB yields breaking new higher highs, I would imagine that investors who were relying on the BOJ-put all along to dispose of their holdings (so, everyone) and were going to dump off to BOJ anyway, would do so ASAP. In that scenario, you would get the opposite of what happened with today’s 1-3Y tenors - far more amount in selling demand than BOJ is offering to buy. And if strong enough, that may then un-cap yields upon itself, the same manner in which markets had capped yields upon itself today, but in reverse.

JGB Trading Supply / Demand

Here is the main and most critical point of this lower than offered amount of 1-3Y JGB selling to BOJ from today.

It is likely not a narrow function of “carry trade” holders, or expectations of BOJ scaling back the amount of purchases per regular buying operation.

What was reflected today is the realities of an incredibly thinly traded, severely liquidity damaged JGB market structure.

This aforementioned chart from Bloomberg…

…is not necessarily showing “a reluctance to sell JGBs to BOJ” as much as it is an inability for BOJ to buy JGBs from investors in the secondary market - due to a structural shortage (or straight up non-existence) of JGBs that are out there to trade in.

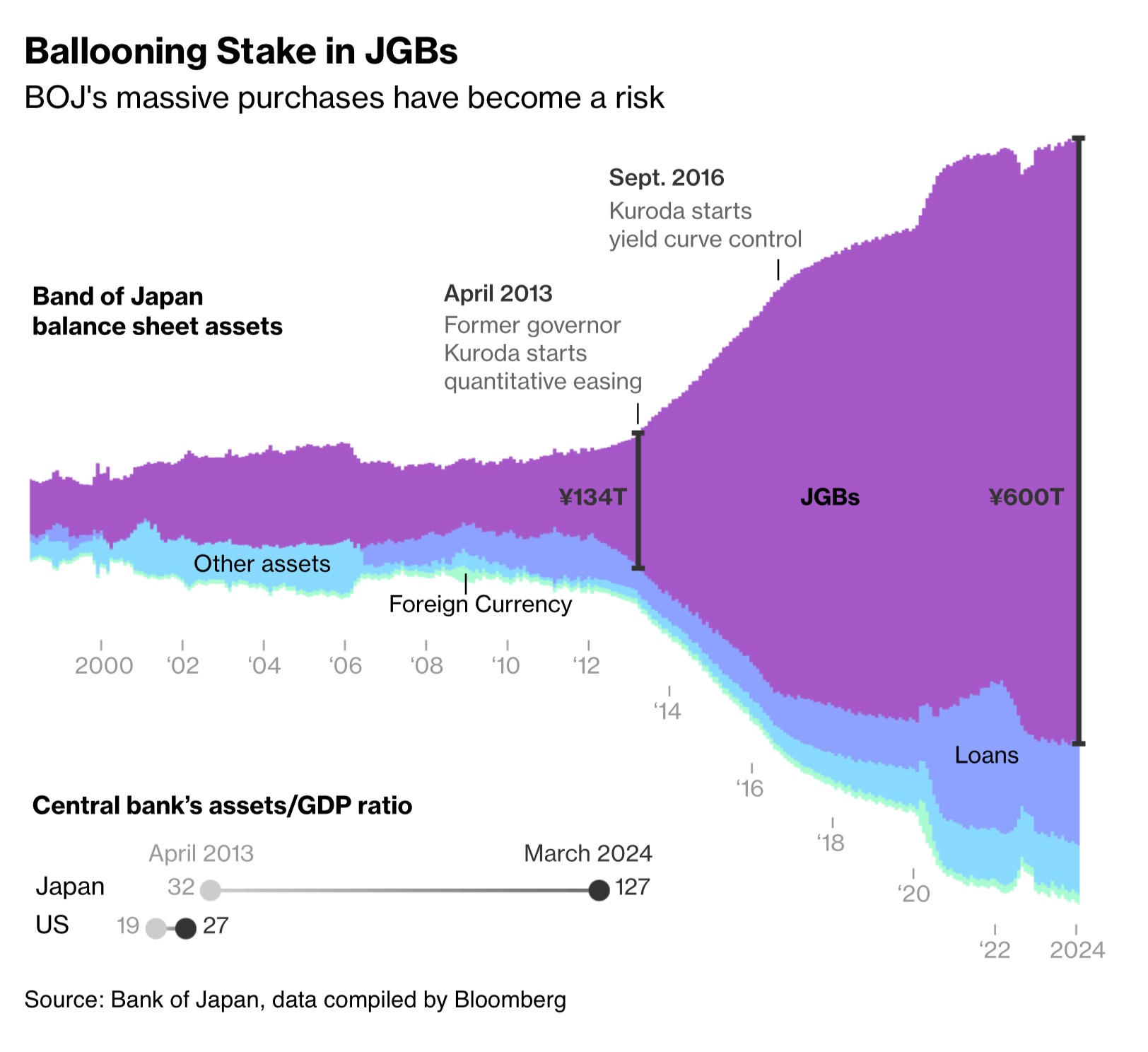

And yes, obviously due directly to BOJ having removed over half of the ¥1 quadrillion in JGBs in existence out of the market via their unprecedented amounts and running length of QQE that is still underway.

If it isn’t clear to anyone out there - the JGB “market” is absolutely not a real market. We can say this with straight confidence by simply looking at these “market prices.” Japan is the world’s most heavily indebted government by a long shot - debt/GDP ratio of more than 250% - nobody else comes close. And yet “somehow” the Japanese government can borrow money for 40 years out at a fraction of the cost of what the risk-free United States government is able to borrow for 4 weeks? Give me a fucking break.

So no, 10Y JGB yields at 1%, or 2Y JGB yields at 0.3%, or 30Y JGB yields at 2% or any of them - those are not real prices if left to free markets. In inflationary times or deflationary times. And similarly, the JGB market is also not a deep, liquid and robust market for transacting in either.

Structurally Damaged Bond Markets

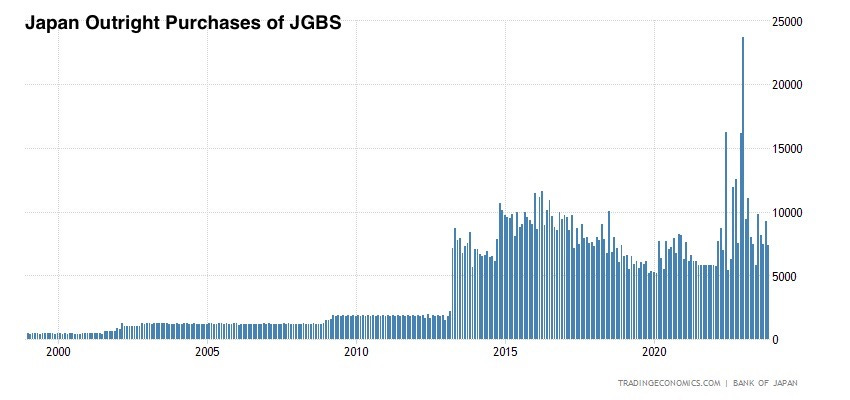

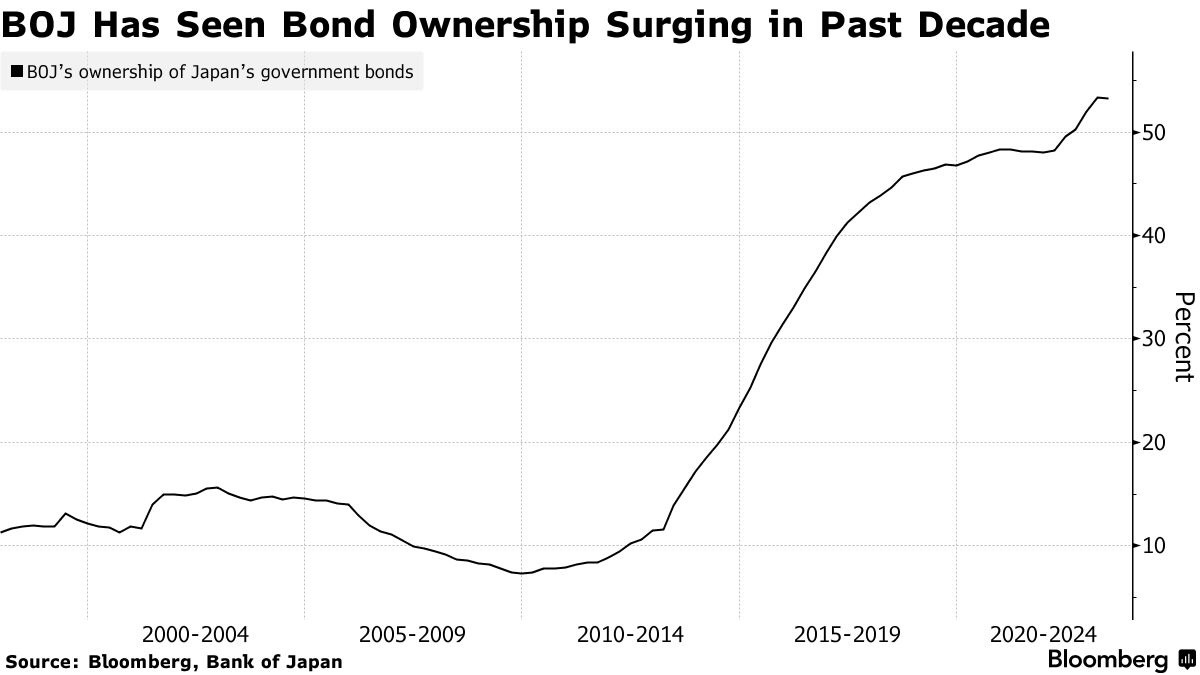

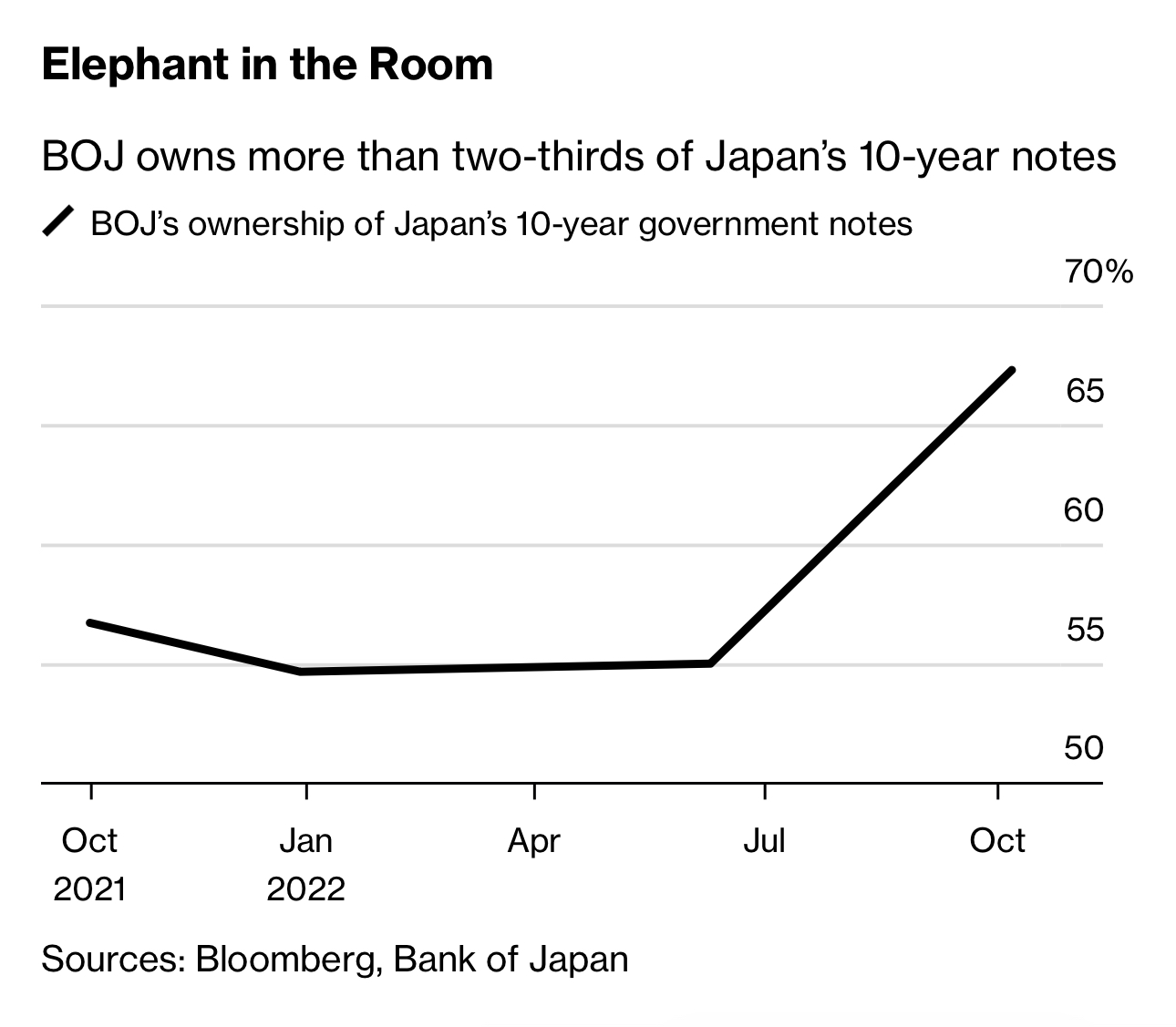

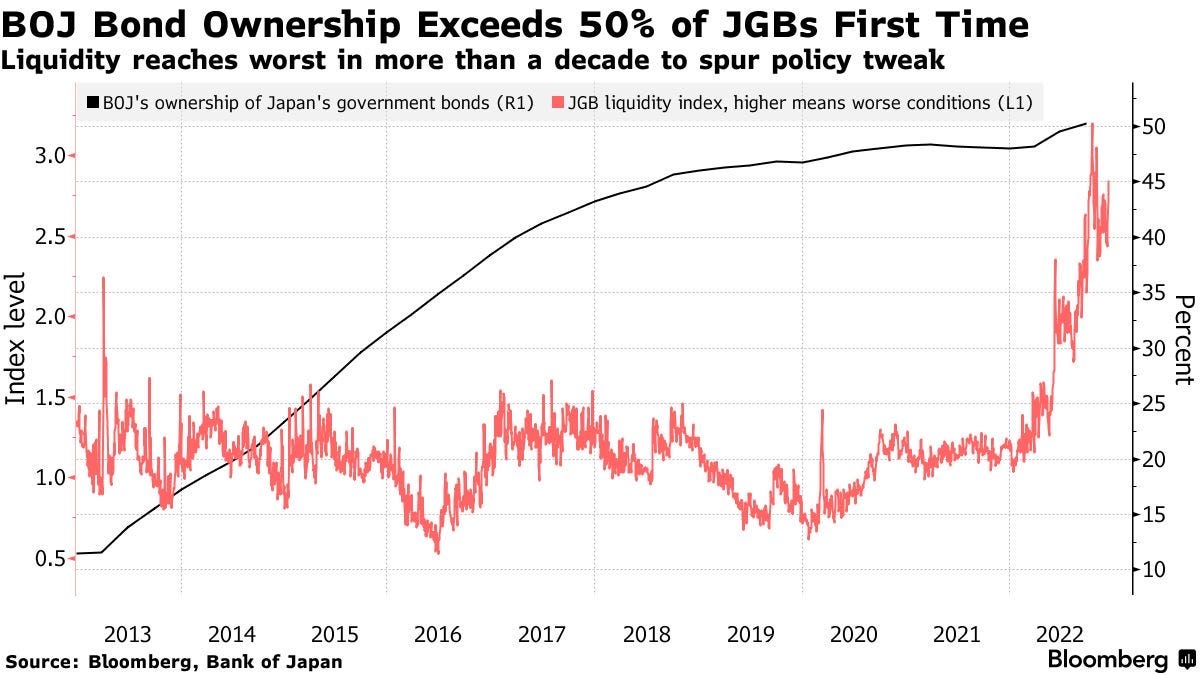

When you have the central bank running QE for over a decade, and at the same (if not an increasingly more rapid) pace of buying government bonds to never be sold back into markets, you are simply removing them from circulation and draining the shrinking physical supply of issues that are available to trade.

When you see charts and graphics like this (or any iteration of)…

…what you’re looking at is how many JGBs have been removed from the pool of supply that is available to actually trade and transact in.

World’s most structurally malfunctioning major government bond market

Although they’re all very bad, 7-10Y JGBs have the worst liquidity profiles for trading, because of yield curve control that had specifically targeted the 10Y JGB yield to pin down (or prevent from rising above) a red line in the sand - which was defended via BOJ offering to purchase an unlimited quantity of JGBs in order to hold the hard cap on yields.

Such that you have phenomenons of complete market dysfunction as…

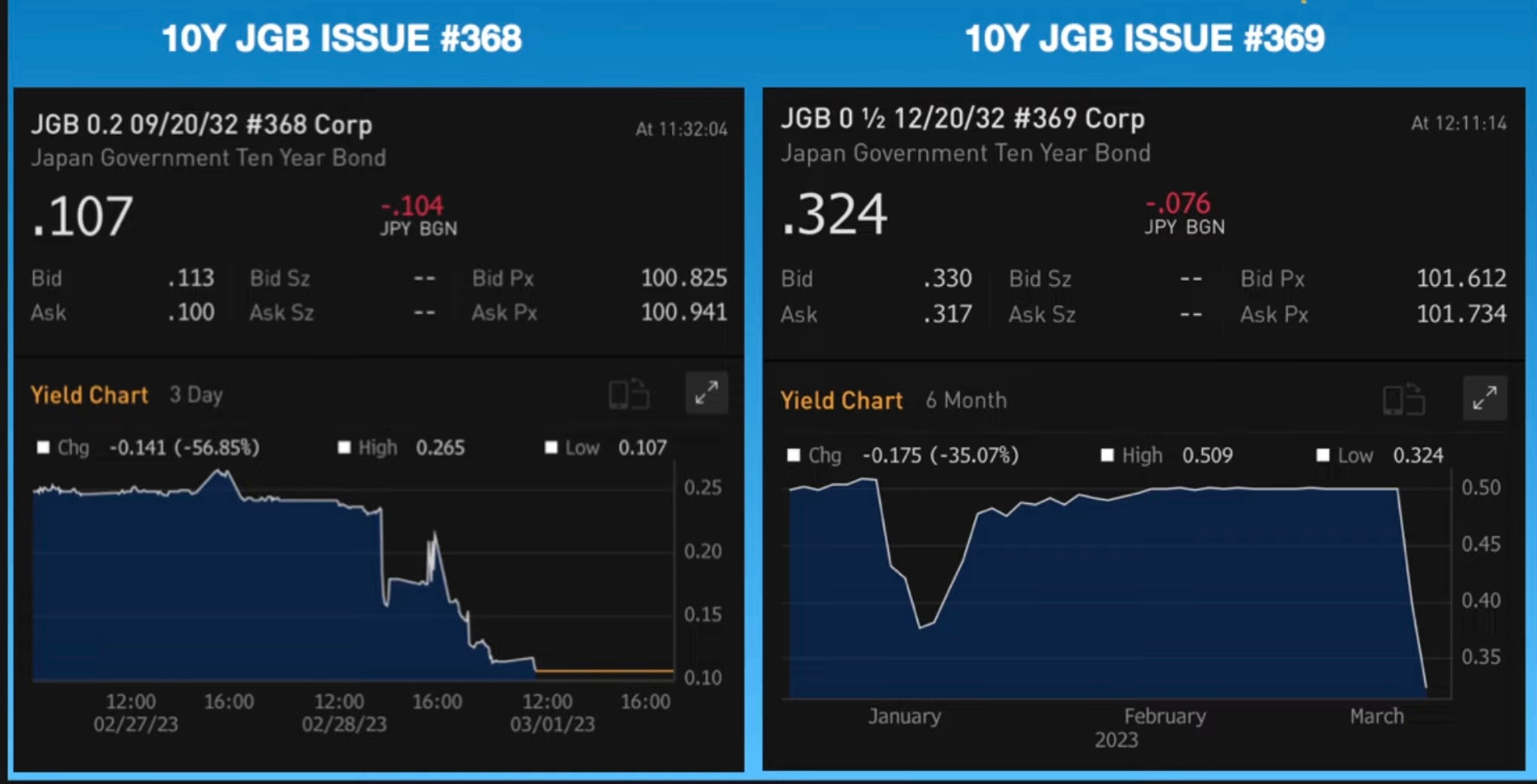

“One bond, two yields” - in which 2 different 10Y JGBs (issue #368 and #369), which were issued only 3 months apart, and thereby should be identical in pricing, had wildly different yields at given moments in time (0.10% for 10Y issue #368, and 0.32% for 10Y issue #369)

And the above is just one example of this happening across many individual JGBs.

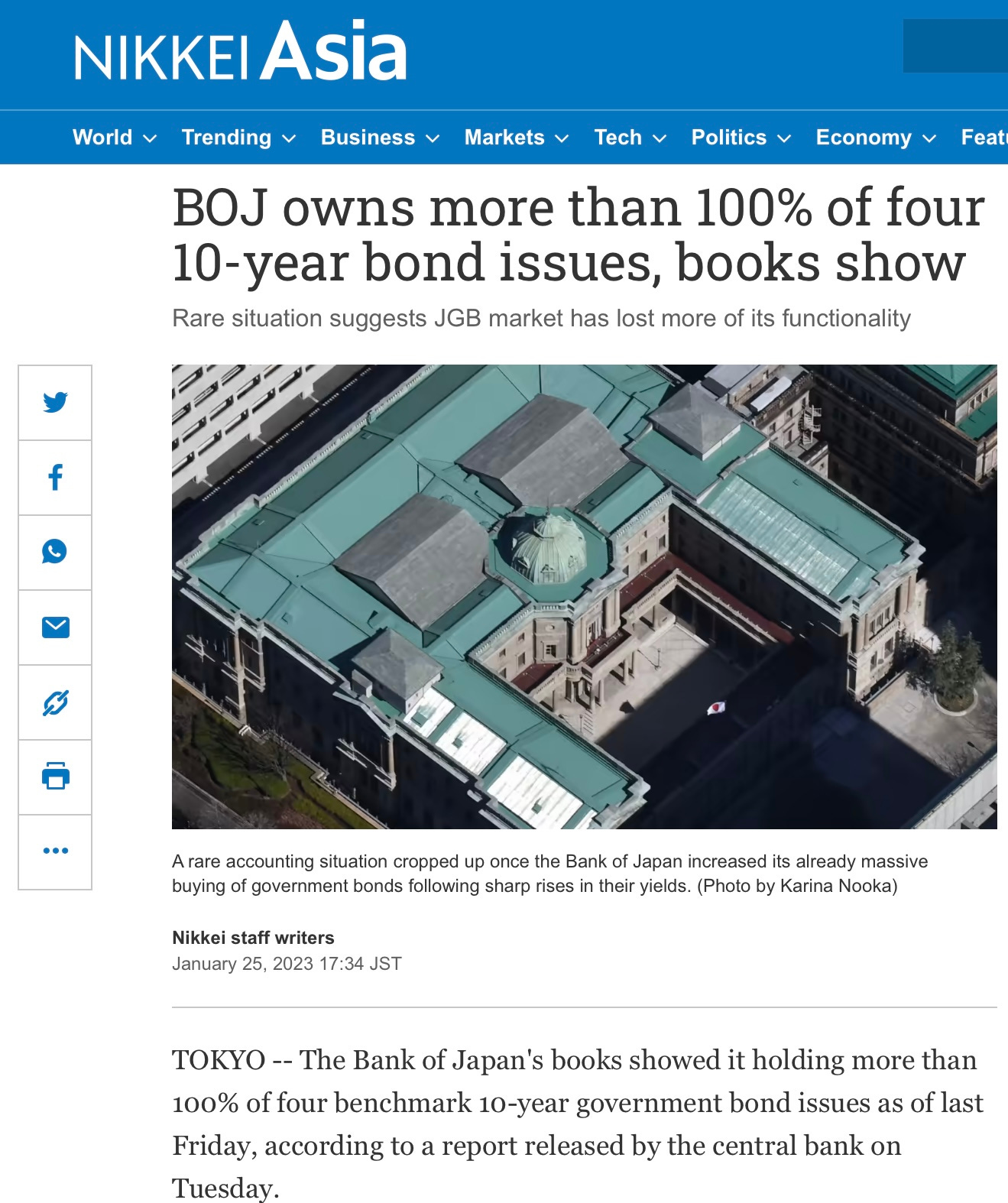

Or- take this example of major market dysfunction - BOJ owning not just 50%, or 90% of any given JGB issue, but in some cases owning over 100% of individual bonds:

…which is made possible because BOJ essentially has bought up all of the existing supply, and then they would also need to lend them out, to then buy back again, thereby “owning more than 100%” on paper.

One can point to these insane things as “side effects” of aggressive, non-stop, and very literally unlimited buying policy- and they are.

How BOJ screws JGB shorts at subconscious (or not) expense of market functionality

But there is also another dirty little trick that BOJ plays in their JGB market cornering game, which is very much a conscious and purposely done motive, not a side effect: targeting cheapest-to-deliver (CTD) issues of JGBs in their unlimited buying.

The very basic explainer is: unlike shares of stock, or futures contracts or other publicly listed and traded instruments, which are each and all the same (1 share of MSFT, or 1 contract of Dec’24 WTI crude oil futures is no different from another of the same green and red blinking ticker), bonds are different from issue to issue. As I showed in the example above, all 10Y JGBs are not the same - they are issued in batches at different times, and therefore have different time to maturities, and different characteristics (though unlike those 10Y JGBs, they should be more or less the same in pricing - or at least a hell of a lot closer than a threefold yield difference).

Say a brand new 10Y JGB was issued today, with 10 years left until it matures (known as “on-the-run” issues - these are the generic yields that you see quoted on Bloomberg or what have you). A 10Y JGB that is say 3 years old is still a 10Y JGB, but has only 7 years left until maturity - and was issued at a time when the prevailing interest rate levels from 3 years ago were not at the same levels as they are when the latest/newest 10Y JGB was issued today. These differences in characteristics among all of the 10Y JGBs in existence make for each issue to have a unique price that may be different from issue to issue any given moment. Some 10Y JGBs are cheaper than others, despite all having the same face value upon maturity. Cheapest-To-Deliver “CTD” bonds refer to literally the cheapest 10Y JGBs that meet the criteria for 10Y JGB futures traders to deliver upon / after quarterly futures expiration - in which those who hold short JGB futures positions after expiry are on the hook to deliver physical JGBs to those who hold long JGB futures positions at expiry.

In 2022, BOJ would not only aim to buy on-the-run issues of 10Y JGBs (in unlimited quantity if necessary), but it also began to directly and purposely target specific CTD issues of JGBs as well in their buying operations - thereby making them not-so-cheap-to-deliver. And who does that negatively affect/screw? Short JGB futures traders (as well as JGB basis traders which I won’t get into now) who would be on the hook to find, acquire and deliver these 10Y CTD JGBs. And going even further - by purposely and specifically buying up CTD issues of 10Y JGBs, BOJ would end up owning and cornering the existing supply of CTD issues.

So now, the soon to become victim of widow-making foreign hedge fund who shorted JGB futures in size, and held their position open into futures expiry (as they were playing a “BOJ will lift YCC bands at the next meeting” - a meeting that would happen to coincide with futures expiry date) would then have to scramble to find, buy and deliver CTD JGBs to fulfill the futures trading contract and close out the trade - but CTD issues don’t exist out there to buy and deliver, because BOJ owns the supply of them. Perhaps not all of them, but a giant portion of them - an amount that has material consequences on those JGBs trading availability.

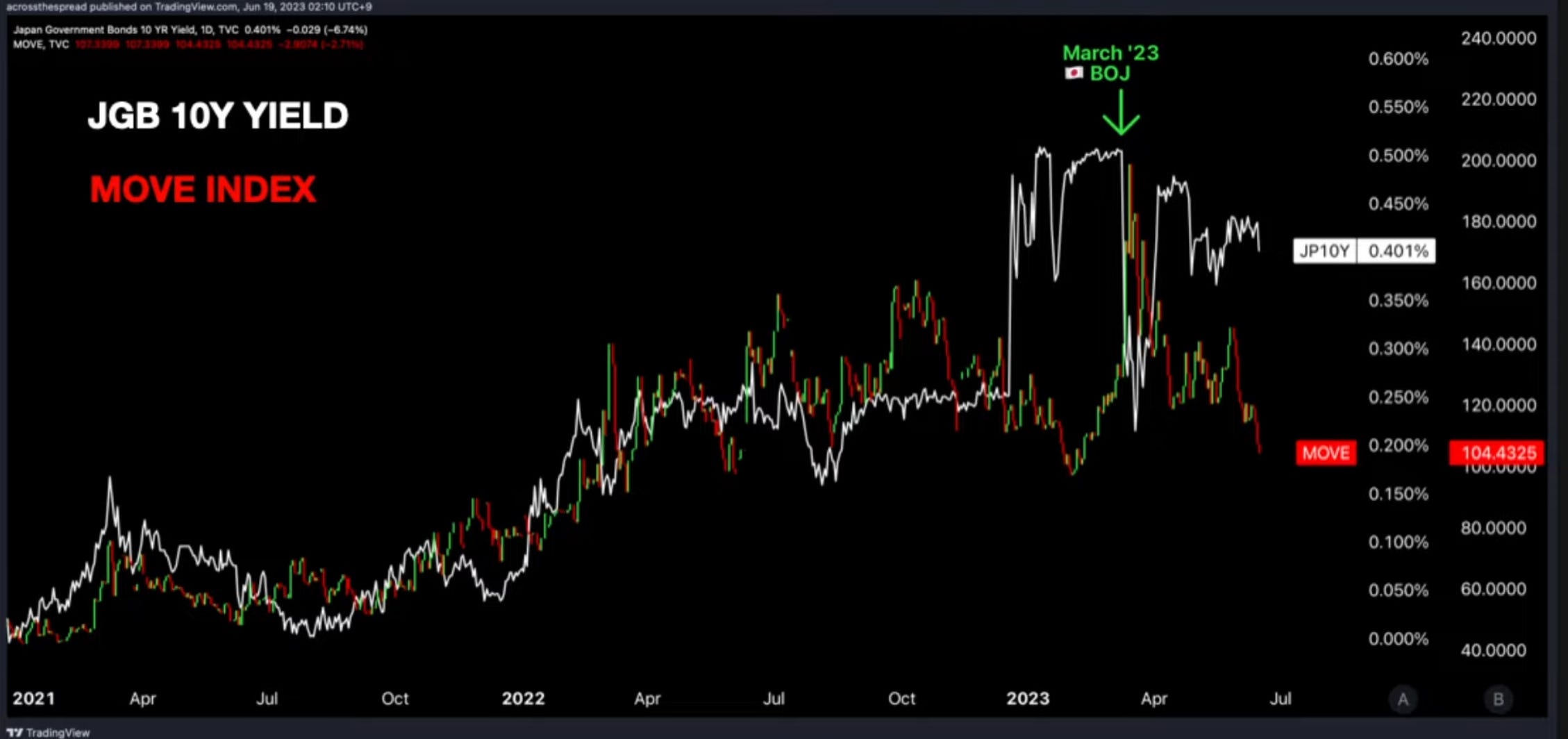

And as mentioned above, BOJ can lend out JGBs that are sitting on their balance sheet to these now desperately scrambling hedge funds (to anyone really) who suddenly find themselves unable to deliver the physical JGBs that they’re on the hook for via the BOJ Securities lending facility - and they will charge a borrowing rate to do so. And in Feb 2023, just a few weeks ahead of both March BOJ and March’23 JGB futures quarterly expiry date for which there was a then-record sized short JGB futures positioning based on expectations that YCC bands would “have to” be lifted, BOJ quietly increased that JGB securities borrow fee by fourfold.

So, shortly thereafter, at the March BOJ meeting- for Kuroda’s final middle finger as Governor of widow-making, BOJ once again did NOT change a single word of policy, let alone YCC. And in the immediate mad scramble for extremely thinly available 10Y cash JGBs by foreign hedge funds forced to short cover their very wrong positioning, 10Y JGB yields got cut by more than half from 50bps (then-YCC cap) to under 25bps (below the prior YCC cap) within 1 ½ trading days.

If you think that the global yield collapse and rate volatility bomb that exploded in March 2023 was solely due to Silicon Valley Bank - it absolutely wasn’t.

It was triggered by BOJ, yes- but the absolutely jaw dropping rate market swings comes from structurally impaired, far less liquid than perceived sovereign bond markets- from U.S. Treasuries to German Bunds to UK Gilts (for which it’s structural illiquidity was already put on display in Sept - Oct ‘22) to Japanese government bonds.

That week in March 2023, foreign investors ended up buying the most JGBs by this cohort on record. And that very same week, Japanese investors bought the most USTs on record. Mutually assured yield hammering. (And in case unclear/not obvious, foreign investors weren’t “buying JGBs” at most-on-record levels as a newly opened long position - they were short-covering and exiting the trade at any cost. Either way, UST and JGB yields get crushed on mutual net buying of each other’s bond markets.

The longer and more intrusive the central bank’s QE program, the worse the trading liquidity profile of its respective bond market - hence JGBs being the epicenter of March ‘23 rate vol that saw the demise of several veteran hedge funds who made a killing during eras of macro hyper volatility (Asia currency crisis, LTCM blowup, dot-com blowup, 9/11, ‘08 crisis, EU debt crisis, COVID etc) but couldn’t seem to handle “SVB collapse.” What they couldn’t handle was the unexpectedly illiquid government bond markets- relied upon to be the deepest and most liquid markets in the world (but were not), and intense level of un-tradeable rate volatility that comes of a giant wave of capital hitting thinly traded markets that only reveal their actual (il)liquidity profiles in real time.

If you want a sense of how unique and truly disruptive this episode of rate vol in March ‘23 was, just listen to this 30 second clip of Goldman CEO David Solomon’s opening remarks for their earnings call discussing that quarter - a quarter in which basically every major investment bank made a killing from the rate volatility except for Goldman, who usually leads in fixed income trading, but instead, had surprise losses while their peers thrived (this is because Goldman disproportionately faces hedge fund clients who were caught in this rate vol storm- the GS trading desk as no exception to being pulled in).

I bring all this up because if you think that “all is well now” with market structure, I assure you it is not. Sovereign DM bond markets are structurally altered (damaged) in their trading profiles and behaviors. This is what is so insidiously misleading about the phrase “normalization” - implying a return to how things used to be before unprecedented and irreversible measures were taken, and I certainly am not singling out Japan here - the clear leader in being the DM basket case outlier as it may be, it is only so because of its lead in demographic decline and national debt levels that force it to have to pioneer these radical policy experiments, which are later adopted (and if not, then certainly considered as an existing option) by peer central banks and governments.

Rate volatility is real, is structural due to central banks overstaying their QE welcome, and is deadly serious with wide scale, real world consequences. Go ask anyone in the UK about how close the entire pension system came to the brink, and how lightning fast and seemingly out-of-nowhere that catastrophe had erupted. And again, what did it take to put the long end UK Gilt inferno out? The Bank of England had to suddenly do BOJ-style unlimited emergency QE in the middle of an inflationary rate hiking cycle. We often use “taking away the punch bowl” type of alcohol and hangover analogies when it comes to easing and tightening. Bank of England’s temporary unlimited YCC/QE on the UK gilt market in ‘22 was the equivalent of an opiate addict on a long painful road to recovery, who then gets mauled by a bear and is hospitalized in critical condition, and temporarily put on paid meds in the middle of the opiate recovery process (and somehow they actually pulled it off). In Japan’s case, the QQE/YCC/artificially low rate addiction and dependency is so engrained that it has become a vital part of its body chemistry - without it, it would die (and with it, it will also likely die, but not in the immediate “voluntary” withdrawal stage).

What the empty JGB buying op tells us

So, full circle back to less than offered JGB selling / BOJ buying. Again, this is a matter of trading mechanics, trading distortions and structurally impaired trading landscapes. It’s a matter of pure and simple supply and demand of tradable securities, or lack thereof.

For years now, we have all seen or heard of entire days that go by where not a single JGB traded - well, the regular JGB buying op today is an offshoot of that.

Furthermore - when we see JGB yields move in a straight vertical line upwards as per recent market trends, we have to keep this thin trading liquidity profile in mind. A market that does not have a ton of depth resting at the bid and ask price is one that can have its price moved significantly, relative to the small amount of capital needed to generate such a move.

It’s one thing for this to happen on some tiny, illiquid and obscure micro-cap stock that some founder is dumping his 30% personal stake, and crushing share prices down double digit percentage points on himself - small/microcap stocks that trade 1k shares in average daily volume are expected to be susceptible to sharp price swings. But its a completely different matter when we’re talking about the world’s second largest DM government bond market, second only to USTs, to exhibit illiquid micro-cap share price action characteristics - because unlike Obscure Inc’s seldom traded shares, the assumption for major DM sovereign bond markets to be able to absorb a sudden flood of capital (in, or out) without some multi-sigma price move is so deeply engrained, particularly and ironically with the veteran rates traders, that such trading liquidity concerns aren’t even at one’s subconscious level. Being able to enter and exit the market without leaving footprints is built into a ton of risk models, automated and manual out there - models that will react when some “once every whatever number of centuries type of move” occurs - and then occurs again the following week. And that’s what makes this dangerous - proactively engaging in a gun shootout by taking false comfort in thinking you have a bulletproof vest on and can take and absorb gunshots to the torso, when in reality, it turned out that your "bulletproof vest”was actually just another NorthFace vest.

Japan, and frankly the rest of the developed world, will have its central bank do whatever it does with monetary policy - hike rates, cut rates, QE, QT, temporary YCC, whatever it may be, in order to fulfill its madate(s) regarding inflation, unemployment, growth etc. But at the end of the day, none of that matters when market instability hits - because that is in the immediate, and requires immediate priority. And that’s really what modern central banks were created for - just look at the history of the Fed - it was born out of the need for market stability and a backstop of last resort. And it remains that way to this day.

In the latest minutes from April BOJ - on the topic of QQE (JGB purchases), none of this is about inflation or growth or employment in the real world economy, and rightly so - what the hell do JGB purchases have to do with year over year changes in cost-push Japanese consumer prices? They don’t have any direct link, because buying / selling JGBs is a green and red blinking ticker matter. And the BOJ board is very aware of this obvious fact, and are approaching it as a green and red blinking ticker market matter regarding supply and demand of JGBs in the secondary market, as they should be.

See for yourself.

Bank of Japan April 2024 Summary of Opinions

•Regarding purchases of Japanese government bonds (JGBs), while the Bank is currently monitoring market conditions after the termination of yield curve control, at some point it should indicate its intention to reduce its purchase amount of JGBs. Apart from this, the daily purchase amount of JGBs should be adjusted carefully by the Financial Markets Department, in response to factors such as supply and demand conditions for JGBs.

•The Bank needs to reduce the size of its balance sheet in order to normalize the amount of its JGB holdings and optimize the excessive levels of its reserve balances. Moreover, given that the gradual increase in flexibility in the conduct of yield curve control led to a smooth exit from the previous policy framework, it is important for the Bank to proceed with reducing its purchase amount of JGBs in a timely manner, while paying attention to market developments and the supply and demand conditions for JGBs.

•One option is to reduce the Bank's monthly purchase amount of JGBs -- which is currently about 6 trillion yen per month -- based on the supply and demand balance of JGBs, with the aim of restoring market functioning. Moreover, it is important to indicate its intention to reduce its purchase amount of JGBs from the perspective of enhancing market predictability.

May 9, 2024 Bank of Japan Summary of Opinions at the Monetary Policy Meeting on April 25 and 26, 2024[PDF 394KB

The above is not what I’ve cherry picked - these are the entirety of the comments on JGB buying that were published. This is why you never ever hear me dive into and dissect the latest CPI data, or whatever non-blinking ticker direct matter.

Negative rates, yield curve control, JGB/ETF/corporate bond buying, and even yenterventions- these are direct market operations, and therefore need to be assessed on a market based approach. Not because I say so (who cares what I think) - but because those at BOJ themselves are doing so.

And now, bond markets may have just flashed a new red warning light, or a reminder of impaired functionality, but at the very least - a revealed miscalculation or a mismatch in the understanding of the current state of market behavior by the Bank of Japan. A misunderstanding by policy officials occurring in the market that happens to be the most top-down policy cornered and dictated in the DM markets world: JGBs.

I talk about many of the aforementioned topics in this article in my recent guest appearance on the Endgame podcast with

which I suggest you watch in full if you haven’t seen it - discussing yenterventions, BOJ, YCC, potential long term end-game scenarios and more.Thank you as always,

Weston

This article is unlocked for anyone to read and share. If you would like to support Across The Spread directly and help us grow, please consider joining as a paid subscriber for original, differentiated, and global market-relevant insights and commentary out of the Asia Pacific region.