Regarding the June 2024 Bank of Japan policy meeting, for which there seems to be some confusion in interpreting what happened - read my note from earlier today, published before BOJ announced policy and the subsequent Governor Ueda press conference, as that turned out to be a detailed explanation of what had ultimately transpired.

My core point and approach heading into this BOJ meeting announcement, which is one that is far apart from the broad misinterpretations currently occurring out there, is as follows (string of excerpts from my earlier note below):

(from “Thoughts and commentary heading into June Bank of Japan”)

Now, just because this is what the communication will be (a continued reduction of JGB purchases going forward), it doesn’t mean that this particular measure can be decisively translated into policy - or for the markets to have anything solidly empirical to price in some new reality.

How would they communicate this into policy language?

How would we know that BOJ is actually going to taper their JGB purchasing amount in succession going forward, given that JGB regular buying operations are preannounced via a schedule that outlines an approximate range in buying quantity that is released on a month-to-month basis, with the exact details of each JGB buying operation determined and revealed on the day of - all of which is dependent upon and subject to current market conditions?

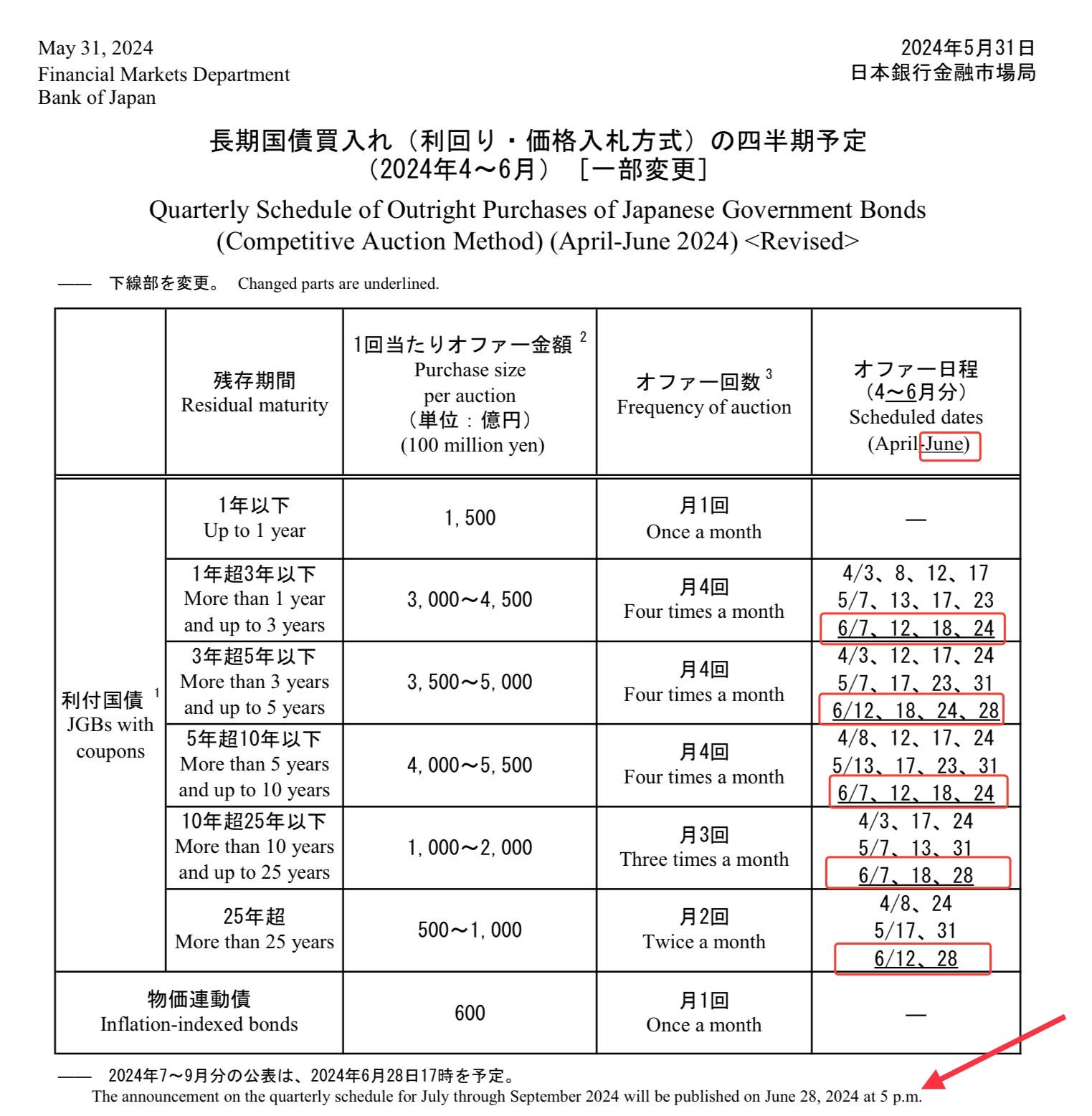

Here is the current JGB buying schedule, which we are still in the midst of.

The next revision doesn’t come until June 28th. But even if they re-published an entirely new schedule mid-month for June effective immediately, as I mentioned - this structure and existing JGB buying protocol in and of itself is one that is designed to be flexible day-by-day. So even if they scrapped the existing schedule and re-wrote it with far lower purchase sizes, it will require a degree of blind faith by markers that BOJ will unconditionally adhere to those lesser amounts of JGB buying. If markets do give the benefit of doubt to BOJ, and somewhere down the line, JGB yields go on a non stop surge, requiring BOJ to violate this “tapering” and buying more than expected (let alone if they ever conduct a fixed rate op bidding for the quantity of unlimited) - they’ve forever lost their ability to pull policy forward.

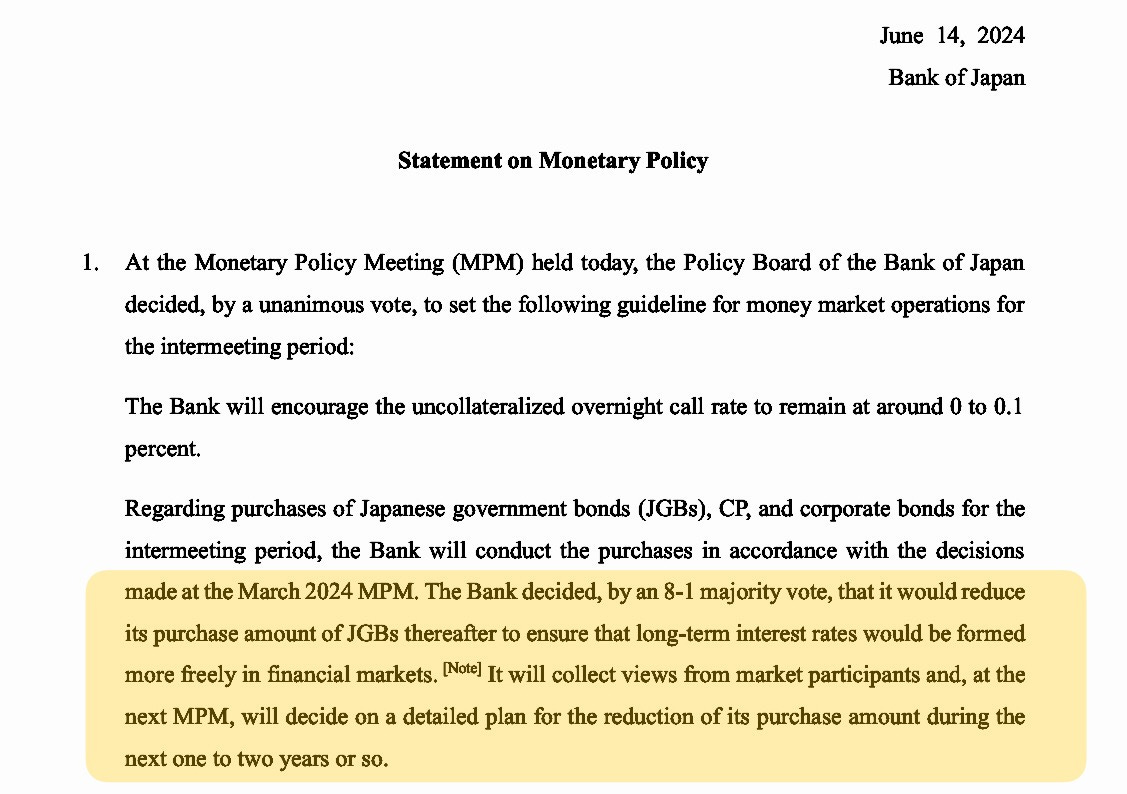

…and here is what had actually transpired from BOJ's official policy statement:

Highlighted

So indeed, BOJ announced cuts to JGB buying today, BUT - without giving any detail whatsoever - details come at the next policy meeting in July.

And what an absurdly strange thing to say for an official monetary policy statement - why, oh why are they merely announcing that there will be a future announcement to alter the amount of JGB buying at next month’s meeting?

Why not either: a) just do it now/today if they’re going to do it anyway in a month, or b) just shut up for today and announce with actual implementation details next month?

It’s because of what I had pointed out - this existing procedural structure of JGB purchasing operations:

The next revision doesn’t come until June 28th.

THIS is why they need to kill some time (hence “details revealed at the next MPM”) - because they cannot actually do anything today that would be “effective immediately” due to this existing scheduling restriction. They need to wait it out until 5PM on June 28th, when the brand new July JGB buying operation schedule and “Purchase Size Per Auction” amounts can be updated.

And this is why I was saying that unless they scrap the entire framework method of how they’ve been going about executing QQE all along, there is no way for BOJ to actually do anything tangible and materially visible TODAY in terms of reducing the amount of JGBs to be bought - as per…

“…the Nikkei leak translated to an actual policy statement would only amount to hollow ink on paper…”

Its quite simple - just requires a basic understanding of how BOJ actually operates within markets, and then just zooming out to look at the big picture. How else were people thinking this would play out- what did they imagine it would look like?

So, no - BOJ didn’t “disappoint” today at all - they very much delivered on what they had media pre-leaked, explicitly stating there will be cuts to the amount of JGB purchases, and did so timestamped on the record for today’s June 2024 official monetary policy meeting statement release. It’s not BOJ’s fault that nobody bothered to question how this would even be possible, nor is it their fault that so many just blindly assumed that "JGB tapering at June BOJ” = “effective immediately” - a procedurally impossible feat under the longstanding standard practice.

That said, let's also be clear: BOJ was also very aware that the public was by and large being very aloof and surface-deep about all of this JGB tapering talk and media leaking - and they never made an attempt to clarify and make sure the markets were aware that “at the June BOJ meeting” didn’t (and couldn’t) mean “tapering JGB purchases begins immediately upon announcement at June BOJ.”

They knew that they were misleading the public / markets of course - they were consciously doing so very much on purpose. Which is why they had to insert this horribly nonsense excuse of "having to wait until they’ve collected feedback from the Bond Market Group meeting before moving forward with the tapering” that was announced today.

Despite announcing today, they “still need time,” because, according to Governor Ueda:

BOJ'S GOVERNOR UEDA: IT'S APPROPRIATE TO DECIDE ON BONDS IN A PREDICTABLE MANNER.

And here is why THIS is laughably blatant and obvious bullshit.

First of all, these “Bond Market Group” meetings are real things - in fact, among all things to track in order to get a potential read on what BOJ actually watches and sets their policies in accordance with, I rank these bond market surveys (and similar market participant studies) that they proprietarily conduct and publish among the very top of the list of factors that actually influence BOJ policy. The bond market meetings and their findings are far more relevant to the course of BOJ policy than Japan CPI is (not that Japan CPI is of genuine influence to BOJ's policy activity as it is).

Why do I put so much importance on their bond market surveying? Because that is the only force which was able to get BOJ to actually move on policy in over half a decade at the Dec’22 shock YCC upper band lift from 0.25% → 0.5% - this policy shock was in direct response to the deteriorating functionality of bond markets, as their survey published in November ‘22 had revealed.

So these bond market meetings themselves are not nonsense. But BOJ and Ueda citing the need to consult the bond market group before making any changes to the amount of JGBs to be bought? THAT is almost at an insulting level of nonsense.

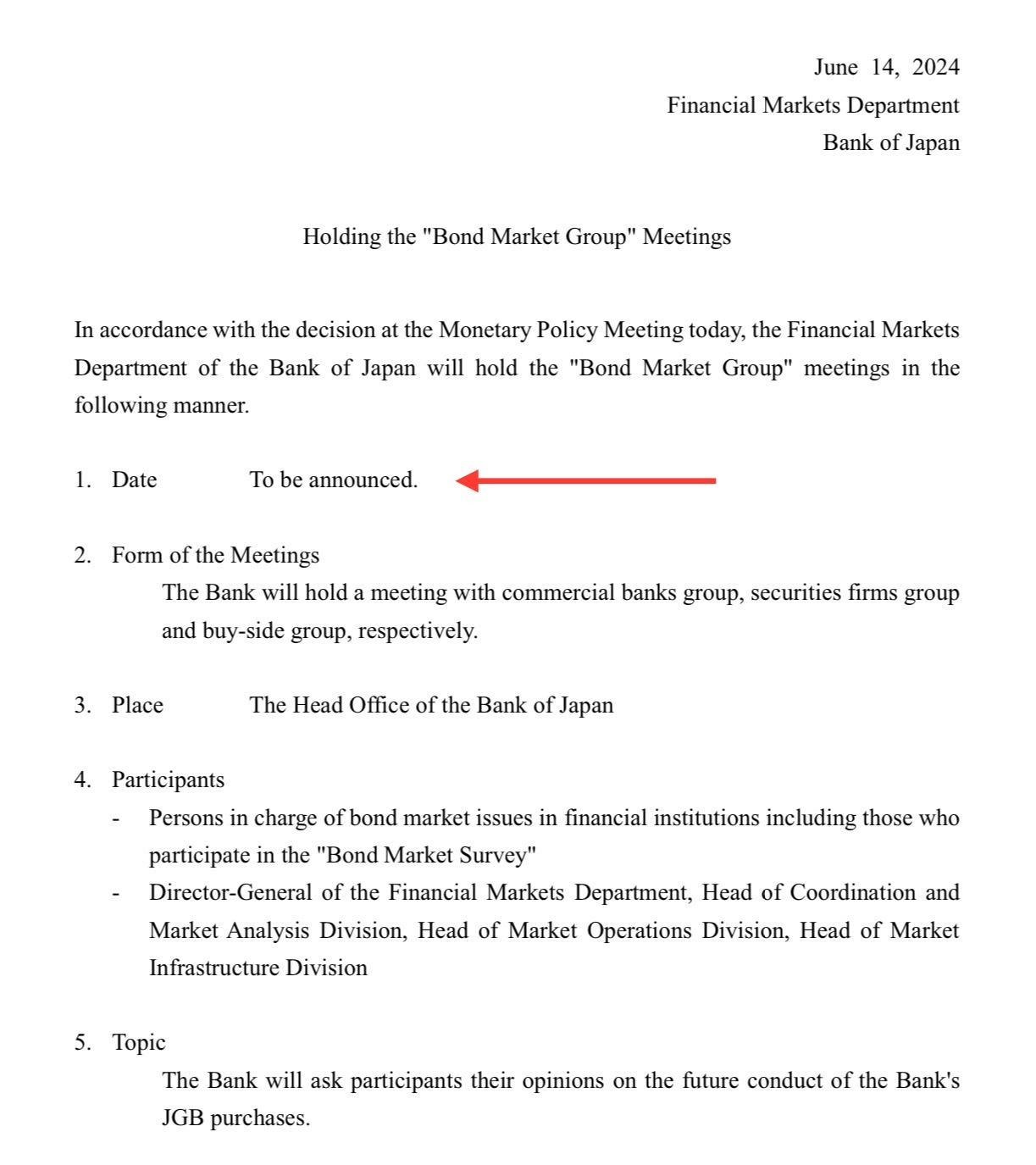

Here is the one other document released by BOJ today, alongside the monetary policy statement itself: Bond market group meeting notice - the “reason” they announced tapering coming, but can’t start quite yet.

Note: Date of this meeting? TBD. Because they just made one up out of thin air today, in order to buy time.

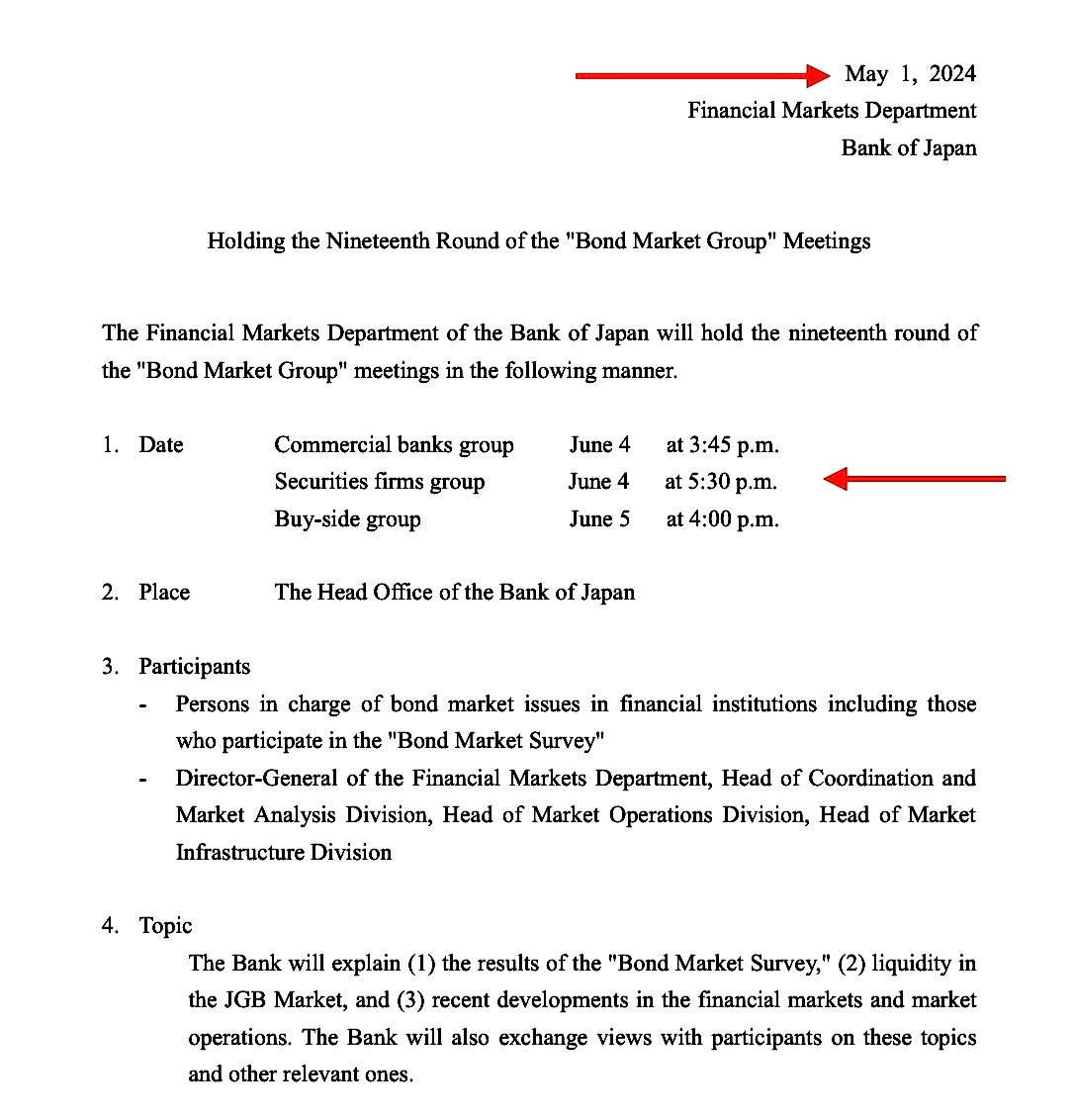

These notices of BOJ’s bond market meetings typically look like the below - and here, I am using the latest one of these "Bond Market Group” announcements (before today’s sudden additional Bond Market Group announcement) - this came out on May 1st.

Notice the time lag between this announcement of the meeting, the meeting dates themselves (about 1 month in between). And then about a month after the meeting dates themselves, BOJ then publishes the meeting minutes and feedback results in another document.

So, the above is the latest document on bond market meetings - published on May 1st, to notify that a routine BOJ Bond Market Group meeting will be held. And when were those meetings held? June 4th and June 5th. That's last week. The bond market group(s) - they just met with BOJ just last week. They haven’t even gotten around to releasing the report of last week’s round of bond market meetings yet- so how long will it be before the results of the meeting that was abruptly announced today, for date: TBD - all of which is apparently what is necessary in order to changing any bond buying quantity?

And really, BOJ, you’re not going to make any changes to the JGB buying schedule until you consult with those of the endangered species- JGB market participants? The very people who will likely be shedding their own JGB holdings and creating market havoc, before attending a meeting that you have convened in which the topic of discussion is “how to not create market havoc when BOJ tapers its JGB buying” ?

For the record, Ueda did say that they can still make policy changes during, or even prior to Bond Market Group Meetings if need be, which includes a July rate hike, according to Ueda. Ok - so, you don't desperately need them then.

And oh yeah - the most blatant reason that this “needing to consult with market participants before cutting quantity” is a hilarious if not deeply insulting level of BOJ nonsense, because of this whole matter of…

May 13, 2024 The Bank of Japan offered to purchase a smaller amount of government bonds in a regular operation on Monday than it did on April 24 as it seeks to reduce its presence in the country’s debt market.

“It’s quite a surprise that the BOJ cut the amount, and that would probably help boost yields,” said Takahiro Otsuka, senior fixed-income strategist at Mitsubishi UFJ Morgan Stanley Securities Co. “It’s hard not to see the reduction as a response to the recent depreciation of the yen. More volatility may hit the bond market.”

Which I personally wrote an entire article about it as well from May 17th, not even a month back

So that’s why this “need to wait and see what JGB market participants say” is such a terribly obvious lie.

And if you watch the Ueda press conference, you will see that everybody sees that this timing and this excuse just doesn't make sense.

Governor Ueda was rightfully pelted with the likes of “Why now? Why not now? Why in July? What’s with this timing? WTF, Ueda? Why? Why??” …by every single reporter at the press conference who was allowed a question. Every single one. Although rephrasing the same question in their own ways. One of the reporters had even got quite unhinged- and just straight up called out Ueda on having an ulterior motive, and accused him of “BOJ is just trying to buy itself some time - but meanwhile JPY is in meltdown" (the dude didn't even have a question for Ueda - just went off on him on live TV at the BOJ Governor's press conference.

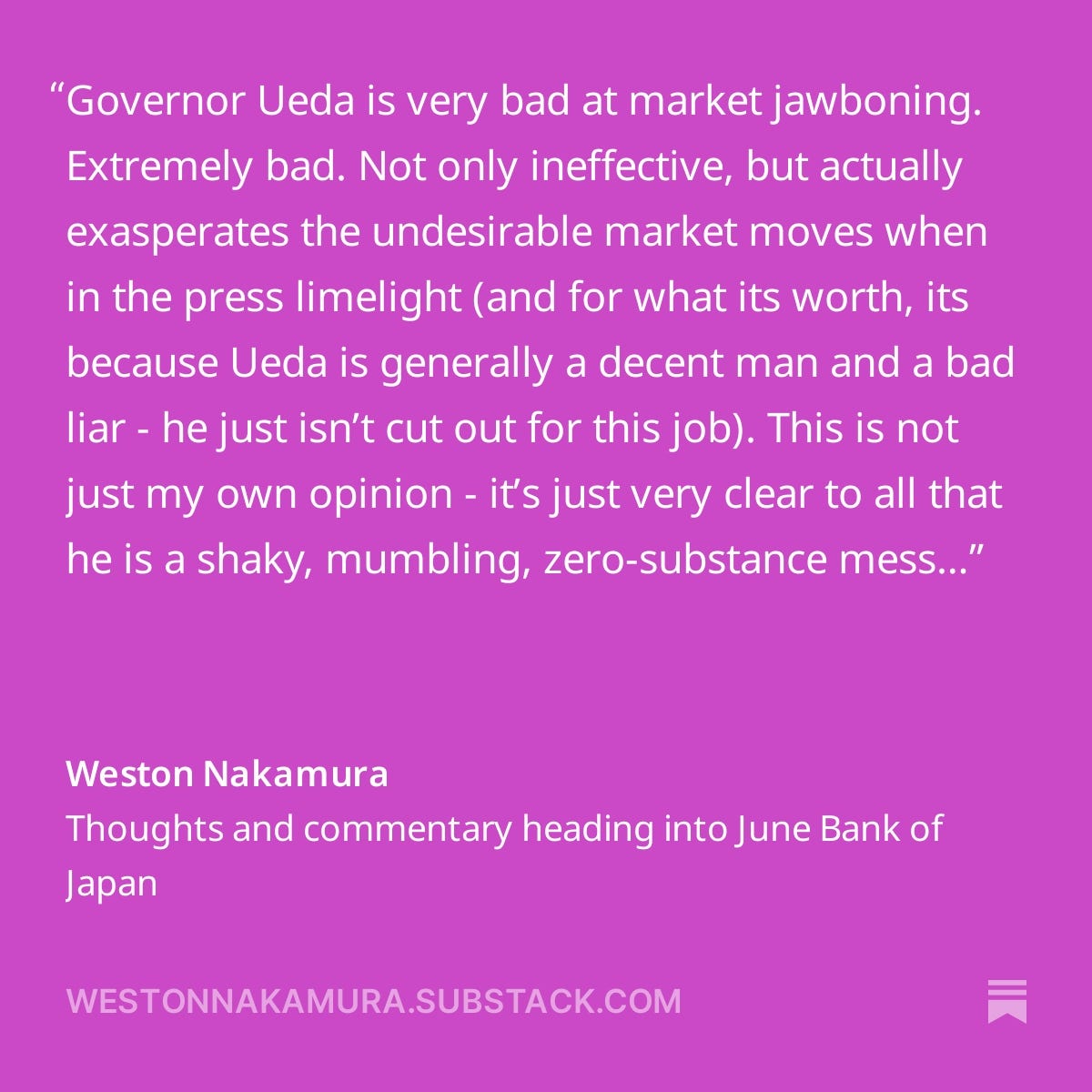

And what did I say in my pre-BOJ note today regarding Ueda's utter inability to perform the art of deception?

So, even my commentary on Ueda being a terrible liar has never been more relevant and significant to BOJ than what was put on display today.

And this misleading of the public narrative for “June JGB tapering” that they were taking advantage of - the reason they were purposely phrasing it that way was in hopes of mustering JPY strength in the meantime. Which actually ended up backfiring on them - if they never pre-leaked tapering policy to start, then they wouldn’t keep getting long and wrong JPY position exiting for USDJPY upside.

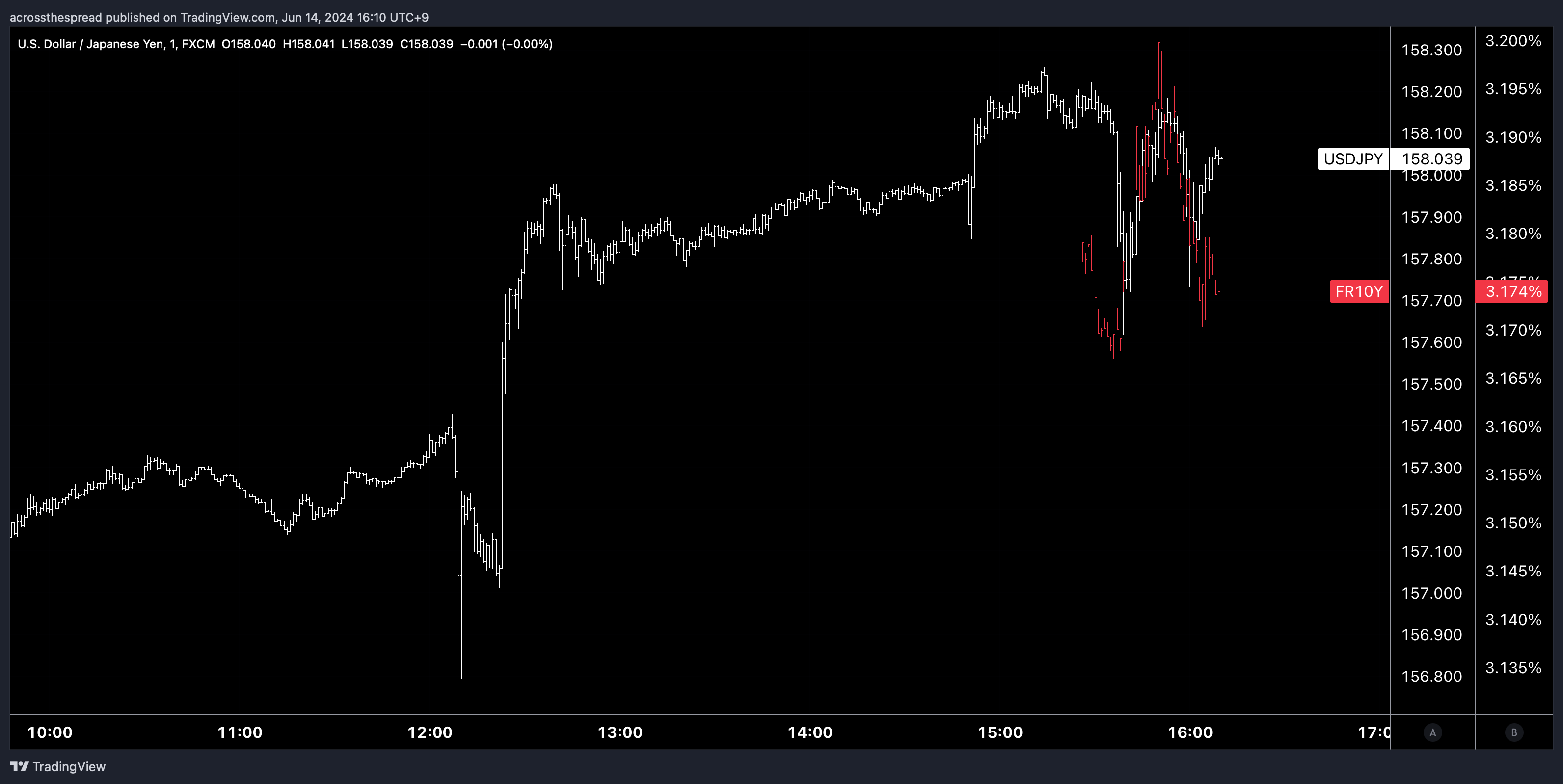

And finally, speaking of green and red blinking tickers - another key reason you saw JPY get hit upon a BOJ meeting (yet again) is because of the confusion and disagreement over the policy announcement - with what I would say appears to be the majority among split consensus views with a takeaway of “BOJ didn’t deliver as leaked/eluded to.”

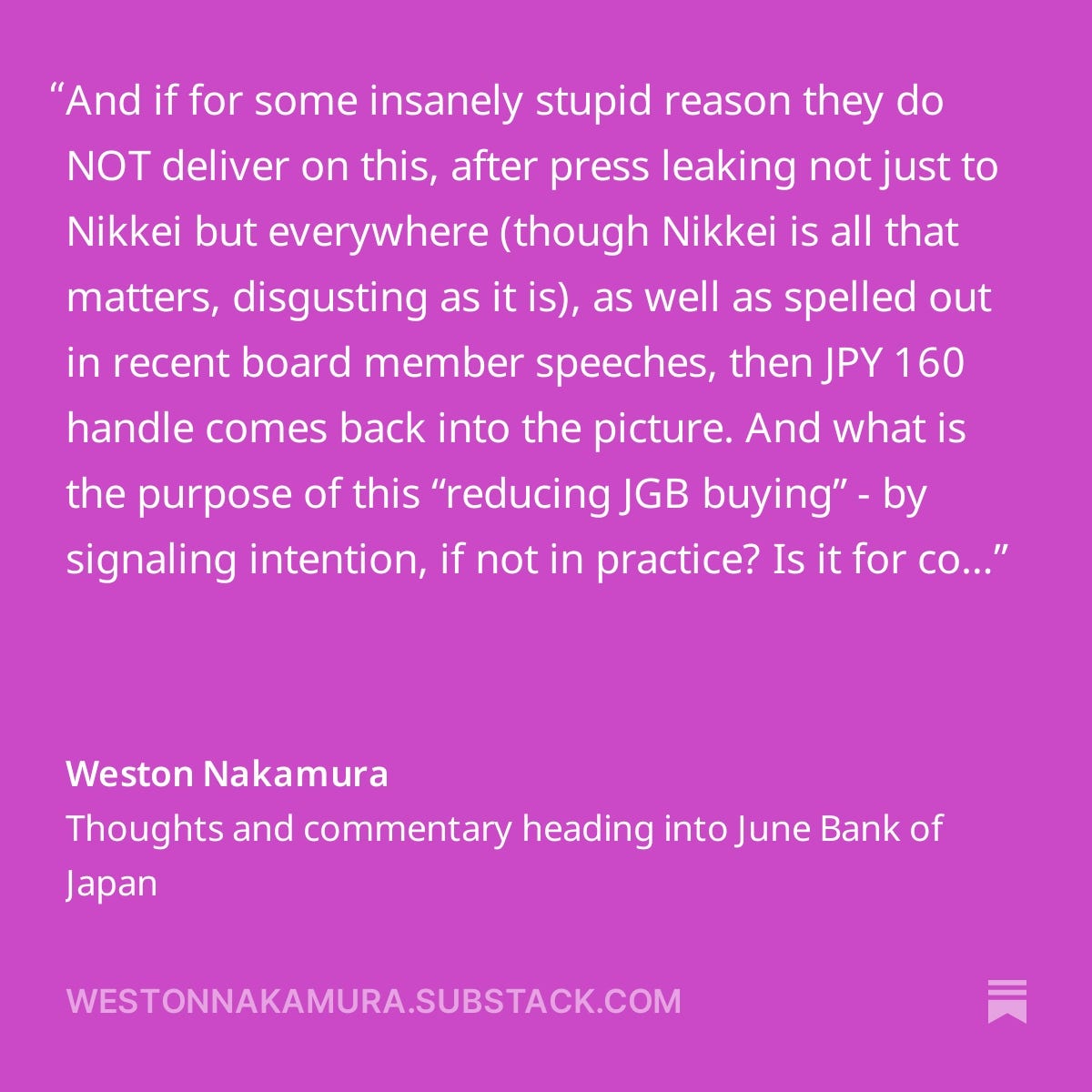

“USDJPY 160 comes back into the picture if this tapering is not delivered” -me

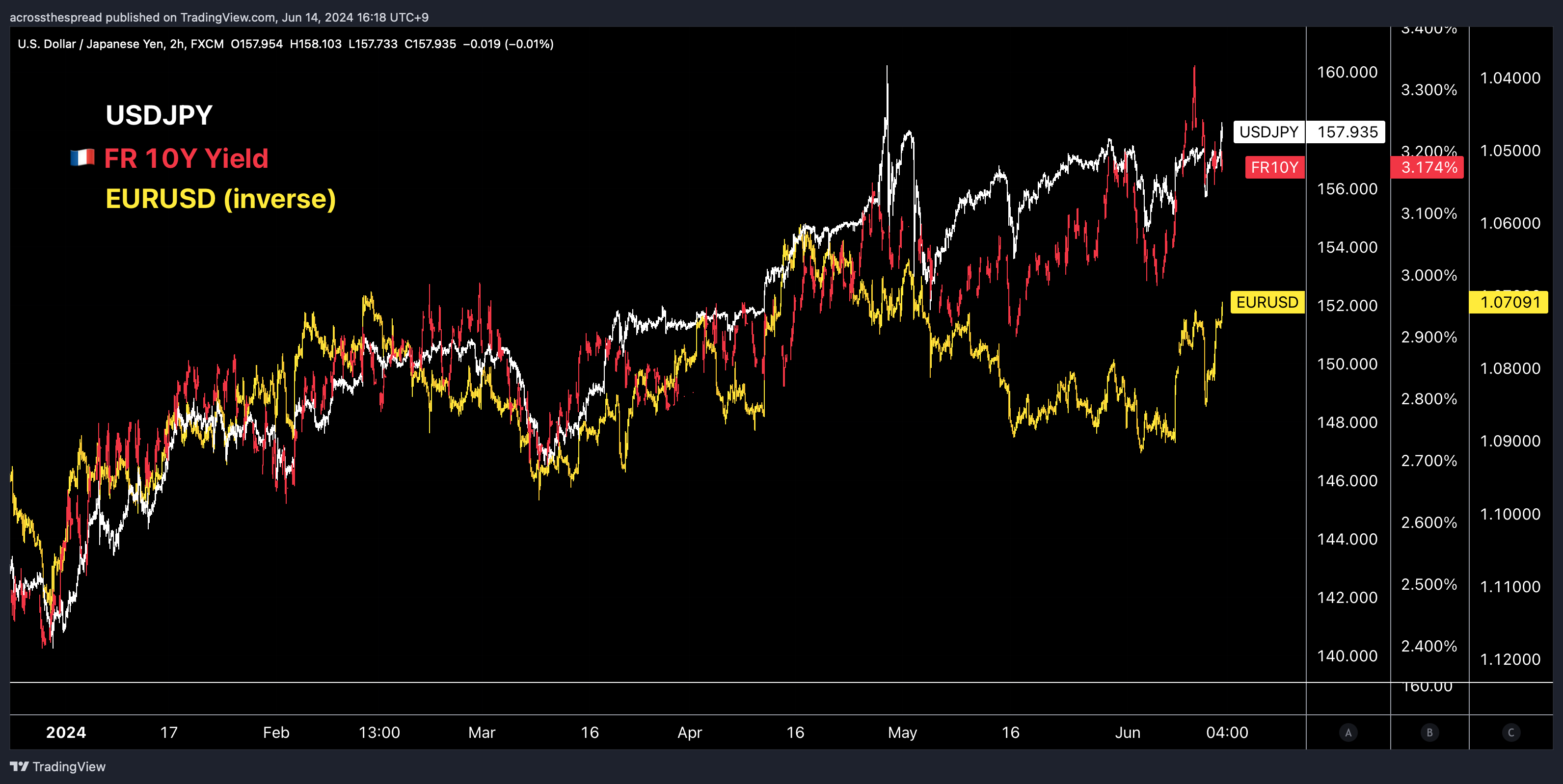

Although, as I mentioned in Substack Notes for short term market observation - USDJPY during Ueda's press conference was once again locked in with French OAT yields, which were still on the rise at EU cash open.

Another delightful tale of BOJ squirming, thx Weston