There Never Was A “Trump Trade” In July 2024 - It’s A JPY Trade

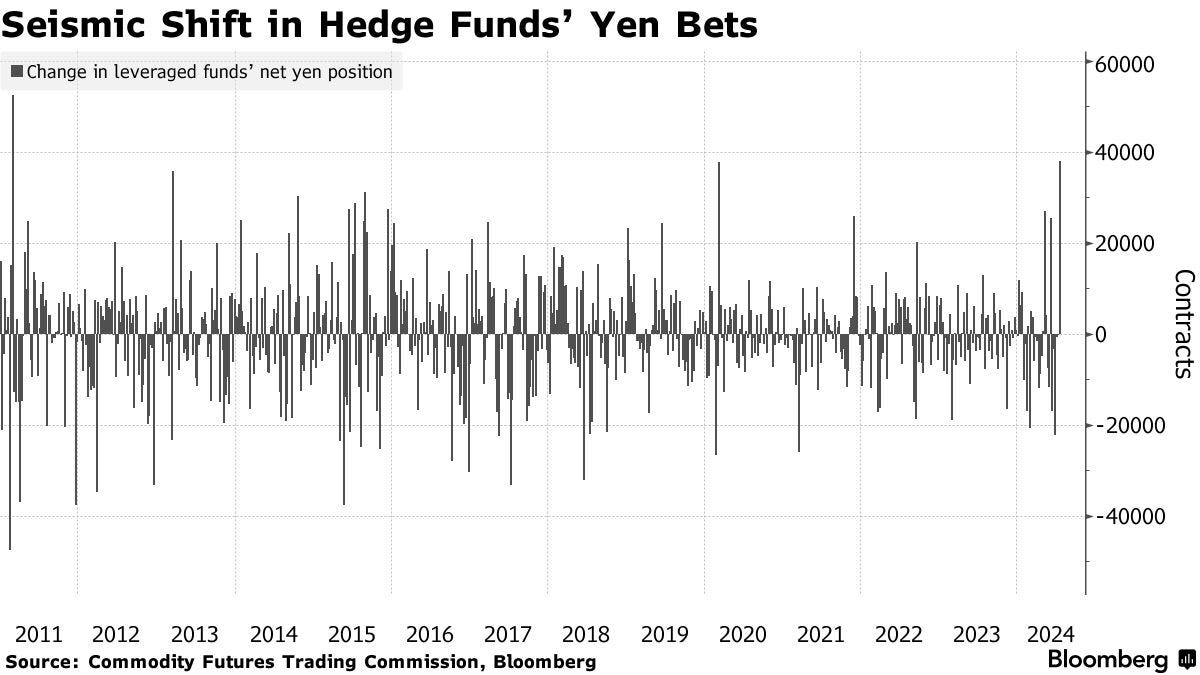

This is a yentervened JPY short squeeze on carry trades and prevailing price trends (crowded positions), with global cross-asset spillovers: NDX, Russell 2K, UST curve, Gold, MXN & more.

There are 3 separate and extensive pieces coming from Across The Spread, under the new format of combining written content with video (4 pieces, if counting the coming note + video on content overview).

Japan Has A New Yentevention Strategy - And It’s Working (For Now)

Elections, Politics, Green & Red Blinking Tickers - The Japanese Foreign Bond Investors’ Role

How the Bank of Japan Buys JGBs

This note touches on themes from all three, but primarily pertains to the first one - the new yentervention strategy being deployed by Japan Ministry of Finance, which will be explained in full depth and detail in the coming article.

For now, this is just some quick market commentary regarding this “Trump Trade” (or the unwind of) that is being discussed out there, in light of the latest developments regarding Joe Biden dropping out of the ‘24 election.

My core message, both in my coming extensive article and now, is simple - there is/was no “Trump Trade” happening in markets over the past week or two.

Yes, maybe certain single stocks are moving intraday on US election headlines - but I am talking about major global macro markets - it is not a “Trump Trade” that has been moving markets, its a lingering JPY short squeeze / short cover and short JPY carry trade forced position unwinding spilling out into various markets, fueled by multiple rounds of MOF yenterventions.

This is the new yentervention execution strategy, in which MOF has apparently shifted from what I call being reactively defensive to now proactively offensive - which began 15 minutes after soft U.S. CPI data on Thursday July 11th at 9:30PM Japan (8:30AM US EST).

Here is my commentary from that post-CPI yentervention moment:

Since then, USDJPY has yet to recover back above 160, hovering between 155 and 158, and getting smacked by series of “mini-yenterventions” - but be they yentervention-induced, or market driven, the sharp and directionally decisive market moves are those that are aligned with (if not pushed by) bouts of JPY strength.

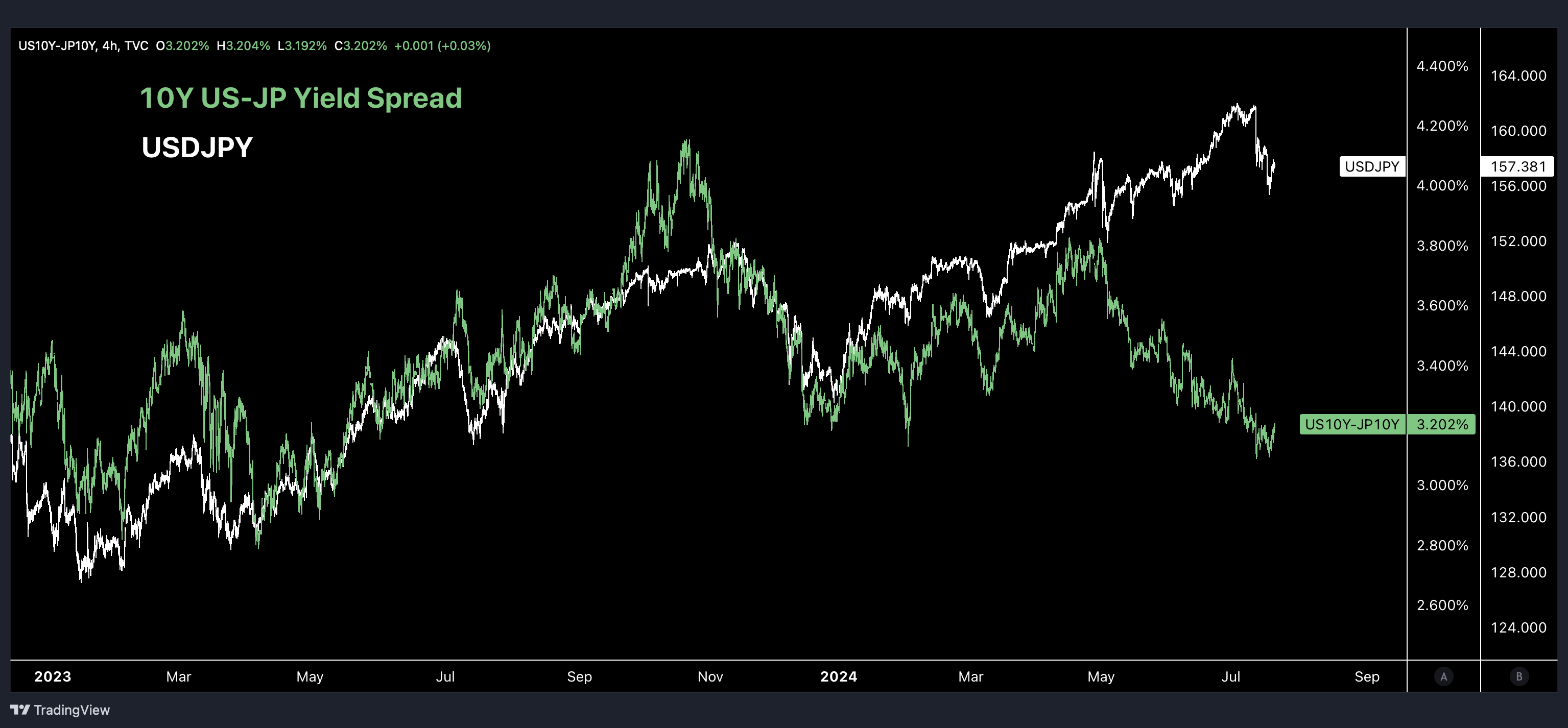

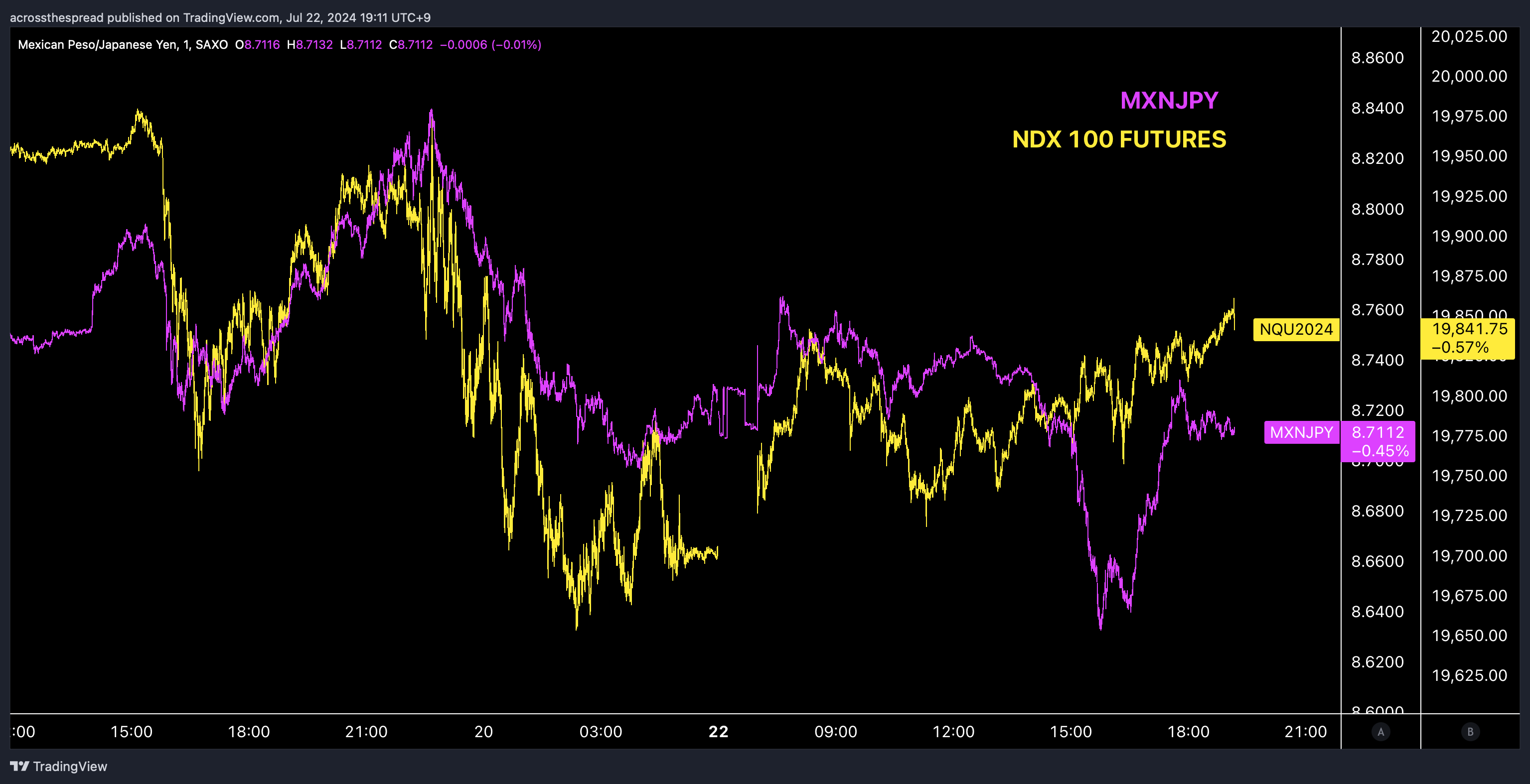

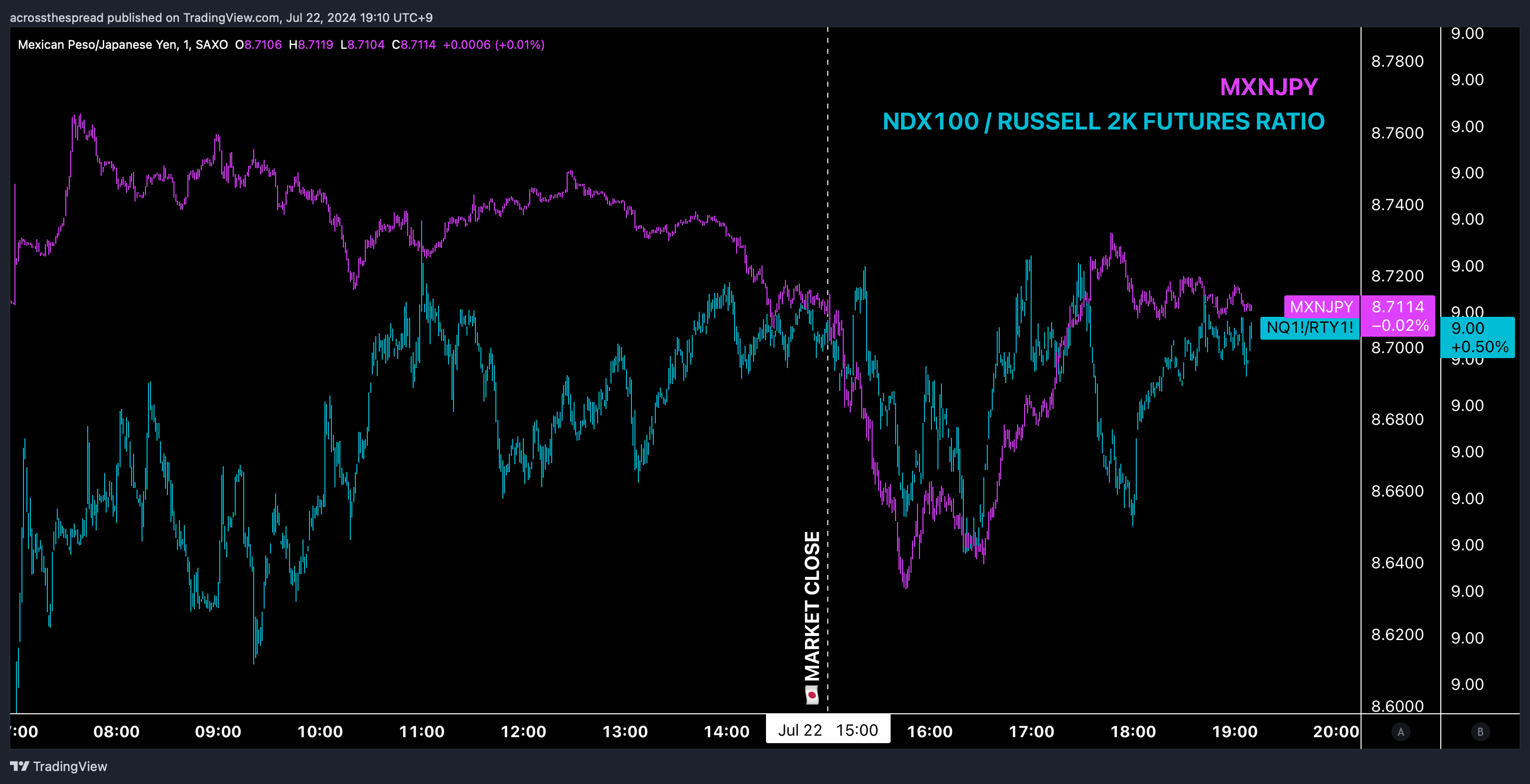

Below are some charts pulled from the coming article on this newly refurbished yenterventionism. As you flip through these, just note the moments of visibly decisive upside on JPY (downside on USDJPY, MXNJPY), and the corresponding asset move in the chart.

Equity Indices

Nasdaq 100 Futures vs USDJPY

FYI, on these charts, the first of the visibly sharp drops in USDJPY is the post-US CPI release yentervention on Thursday July 11th at 8:43AM - meaning, no, they are not moves that occur right upon (and therefore can be attributed to) the soft CPI release moment that occurred 13 minutes earlier (NDX futures actually jumped initially higher upon the softer than expected CPI print at 8:30AM, as one would expect).

Russell 2000 Futures

Long Nasdaq 100 / Short Russell 2000 Futures

Bonds

US 10Y-2Y yield curve “steepener trade”

US-JGB yield spread YTD divergence → recent convergence

Gold

I will also say that broadly speaking, another (non green and red blinking ticker empirical) reason that a clear “Trump Trade” doesn’t currently exist in markets is because the 2024 Trump campaign doesn’t really have any clear, major, idiosyncratic signature economic themes that markets can easily reflect. Very different in 2016 and even 2020 - in those election cycles where Trump was the GOP candidate, Trump campaign had indeed laid out very clear, very specific, and very highly atypical economic and foreign policy agendas - and those characteristics allowed for certain markets to idiosyncratically reflect the market’s constant real-time pricing of a Trump win/loss.

Mex Peso

One such trade / market (especially in 2016 - and for anyone out there who was trading then, as I was, you’ll remember this) was USDMXN. Under Trump’s then-signature “Build a wall and Mexico will pay for it” - the USDMXN FX cross was essentially as pure of a Trump win/lose proxy as anything else - as the USD / Mex peso spot rate was otherwise just some forgotten (but still liquid and 24 hour traded), economically fundamental currency pair. And as such, it therefore was perfect to then become a speculative instrument reflecting then-candidate Trump’s election outcome sentiment (as opposed to say USTs - which are subject to an infinite number of drivers). When Trump upset Hillary on Nov 8 2016 - that day, USDMXN made a +9% intraday move, followed by 2 or 3 more consecutive days of +5% thereafter (if memory serves correct).

Now, fast forward to 2024 - though still running on illegal immigration, Trump hasn’t been touting the invoicing of Mexico as a signature staple of his campaign to anywhere near what the 2016 Trump was doing - and so USDMXN is likewise not the Trump election proxy as it once was (again - another way that “Trump Trades” don’t exist in context of 2016, 2020).

However - as it just so happens, MXN is the long side for one of the most popular and crowded short-JPY carry trades via MXNJPY.

So, while the USDMXN cross has been lifelessly flat in a ±1% rangebound manner since the July 11th post-CPI yentervention JPY surge, MXNJPY has been getting slammed nearly -5% in that same time frame, worse than the -4% USDJPY move, as yenteventions hit the long MXNJPY carry trade and forcing positions to close - which, again, has been spilling out into risk assets.

Below are similar JPY charts from above, but looking at the MXNJPY cross, and updated / refreshed as of current (post-Biden drop out).

MXN vs USD, & MXN vs JPY

Clearly in-line, then clear divergence - but note that when MXNJPY sharply reverses course, MXN’s upside against USD also fizzles out.

Suggesting that the long MXN upside in the first half of the chart was also driven by the MXNJPY cross - USD has almost nothing to contribute to MXN in either direction.

MXNJPY vs NDX100 Futures

NDX following MXNJPY shows the JPY carry trade unwind on display, as well as the “Trump Trade” not on display.

MXNJPY leads NDX in both directions.

MXNJPY vs Long NDX / Short Russell ratio

Snapshot from Asia market open - the first market region that gets to react to any weekend developments.

And by the way, Mex peso is by no means immune from election triggered volatility - recall the massive -5% intraday MXN selloff in early June upon a completely non-shock Mexico presidential election result of AMLO continuity candidate Claudia Sheinbaum win.

Heads Up: Major Carry Trade Unwind - Mex Peso

Mex peso is getting hammered right now, particularly against JPY. Market reaction is being attributed to the election victory of Claudia Sheinbaum by a 30 point margin and a ⅔ supermajority legislature of the ruling party of outgoing President AMLO - despite her win being largely expected, and the newly re-elected government of the existing ruling party, as the view seems to be one of an “unchecked, anti-business” agenda in store.

So USDMXN being relatively rangebound throughout the last 2 weeks, while MXNJPY plunges -4% not only displays the JPY strength driver - but it also highlights the complete lack of the “Trump Trade”.

I don’t know how exactly one can clearly and empirically observe market movements that would be tied to the opening and/or closing of a “Trump Trade” (that’s sarcasm - you can’t empirically measure or observe that which is not a green and red blinking ticker’s scale and timing impact upon green and red blinking tickers).

So, what’s behind the strange cross asset global market moves in the past 1-2 weeks?

JPY short covering, carry trade unwinding, and from the hands of Japan MOF. So this is just a heads up / explanation of what’s actually going on, in case this “Trump Trade” talk vs actual markets doesn’t seem to add up to you- you’re on the right track, just filling in the holes.

Stay tuned for a series of major releases coming - and thank you as always.

Weston

Weston, thank you for your precise input as always. So, do you think that the BoJ's plan is to keep the JPY under 160 with many small interventions before making a big move at the end of July's meeting and finally manage to reverse the long-term trend? It seems that 160 is really the level they want to defend at all costs. Thank you.